FinancialGungHo Online Entertainment

Notice Regarding Dividend from Retained Earnings: Japan

2 pages~3 min full read

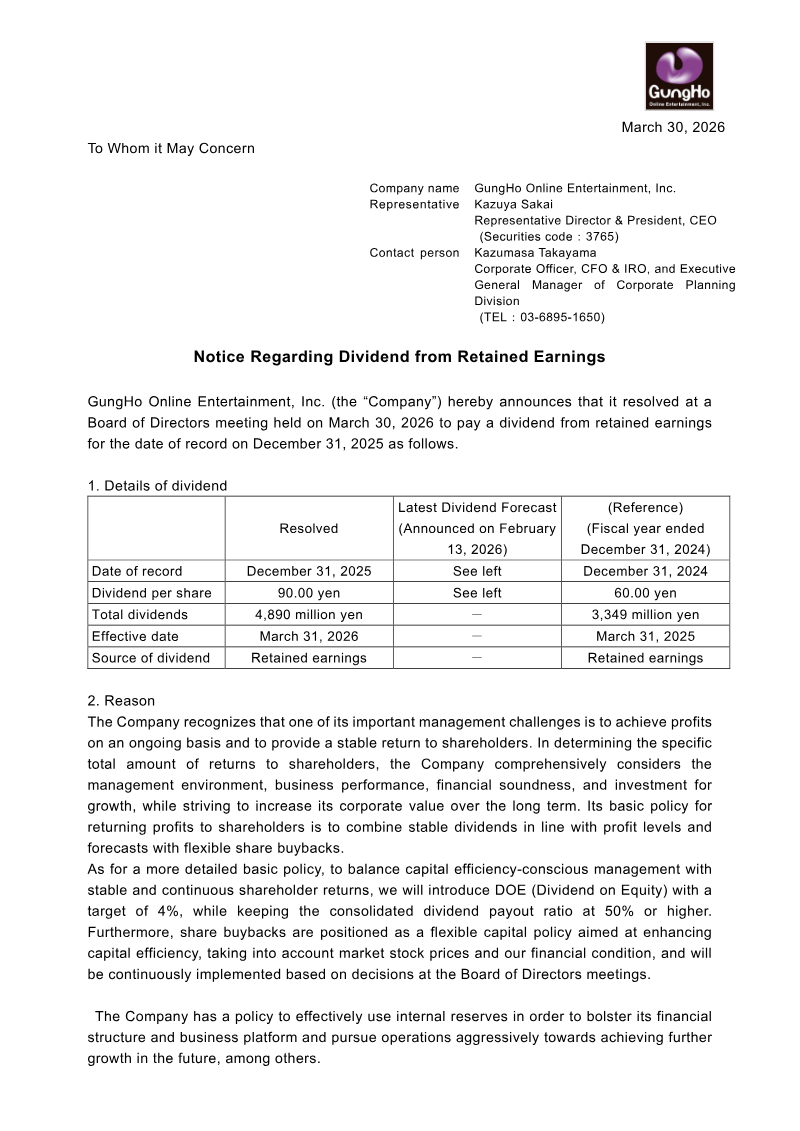

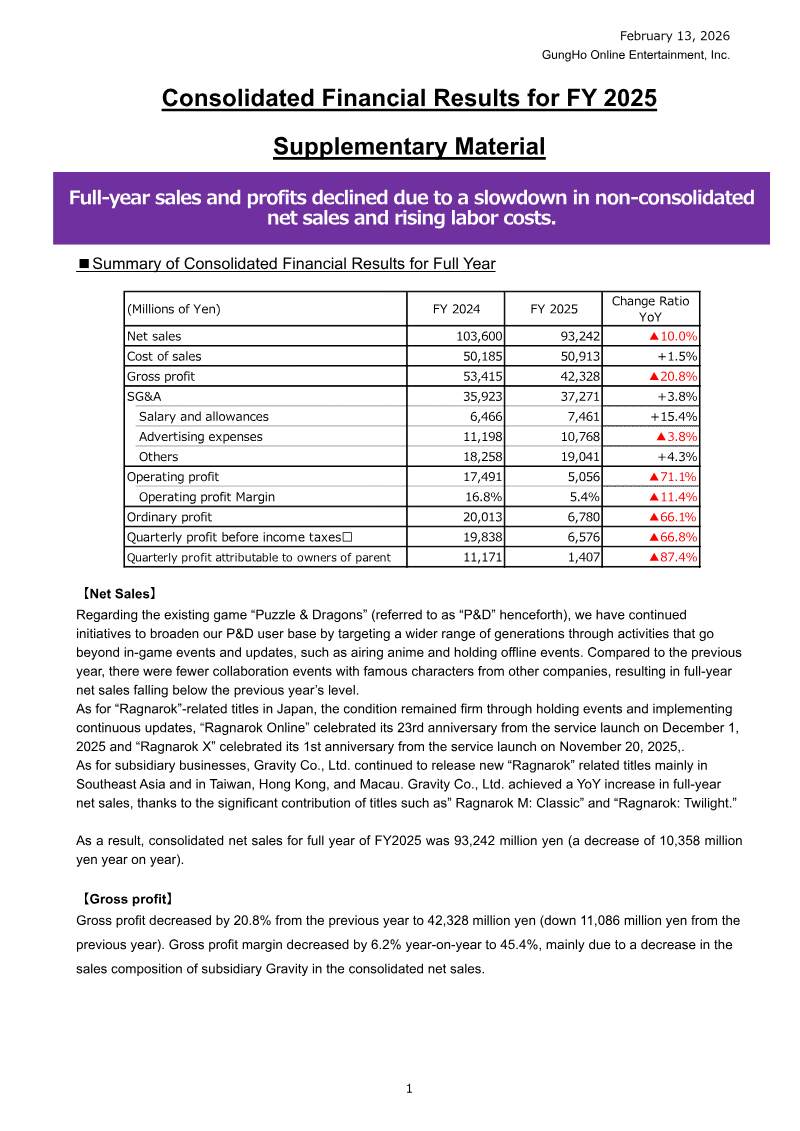

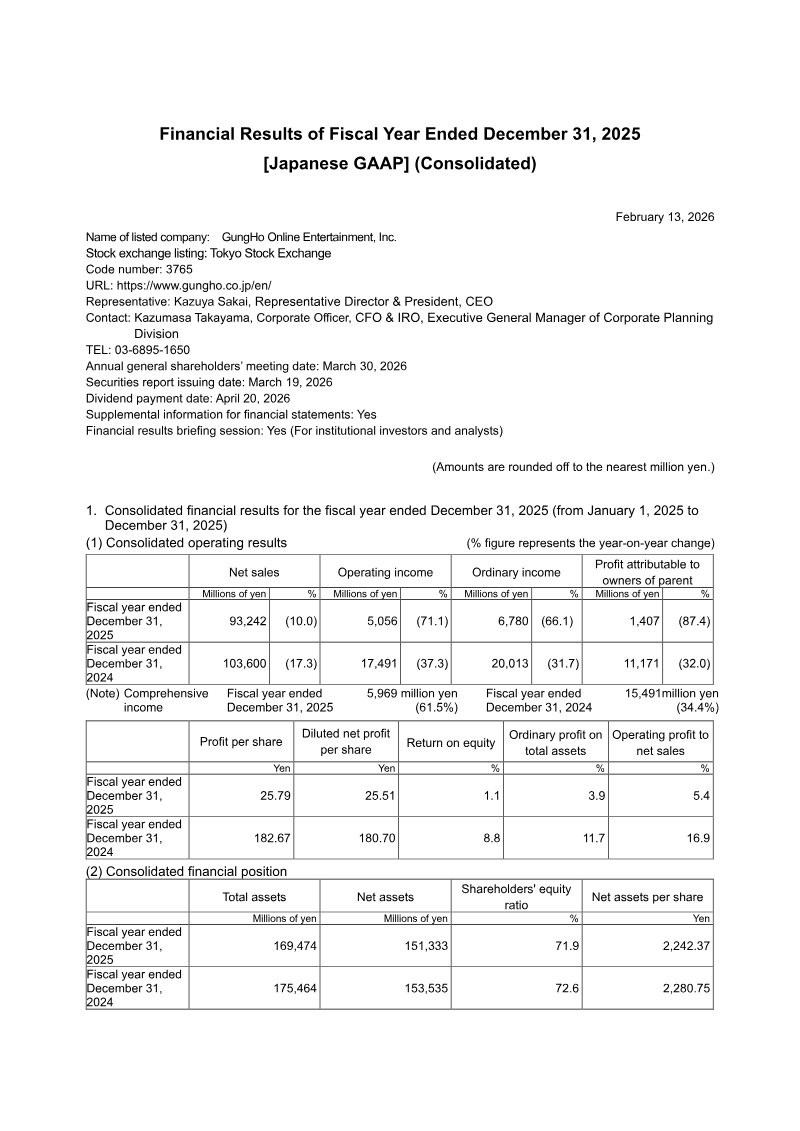

GungHo Online Entertainment, Inc. has formally resolved to distribute a dividend from retained earnings for the fiscal year ending December 31, 2025. The company will pay a dividend of 90.00 yen per share, effective March 31, 2026. This represents a significant increase from the 60.00 yen per share distributed for the previous fiscal year, resulting in a total dividend payout of 4,890 million yen.

The decision reflects a strategic commitment to balancing stable shareholder returns with long-term corporate growth. The company’s financial policy prioritizes consistent profitability and the enhancement of corporate value through a combination of stable dividends and flexible share buybacks. To guide these distributions, the company has adopted a Dividend on Equity (DOE) target of 4% while maintaining a consolidated dividend payout ratio of at least 50%. This framework is designed to ensure capital efficiency while providing predictable returns to investors.

Management continues to utilize internal reserves to strengthen the company’s financial structure and business platform, supporting aggressive operational expansion. While the company maintains the flexibility to issue dividends on a semi-annual basis, the current resolution confirms the final dividend for the 2025 fiscal year. By aligning capital allocation with both market conditions and internal performance metrics, the company aims to sustain its growth trajectory and meet shareholder expectations.

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2026

GungHo Online Entertainment · 2024

GungHo Online Entertainment

GungHo Online Entertainment

GungHo Online Entertainment

GungHo Online Entertainment

CyberAgent · 2026

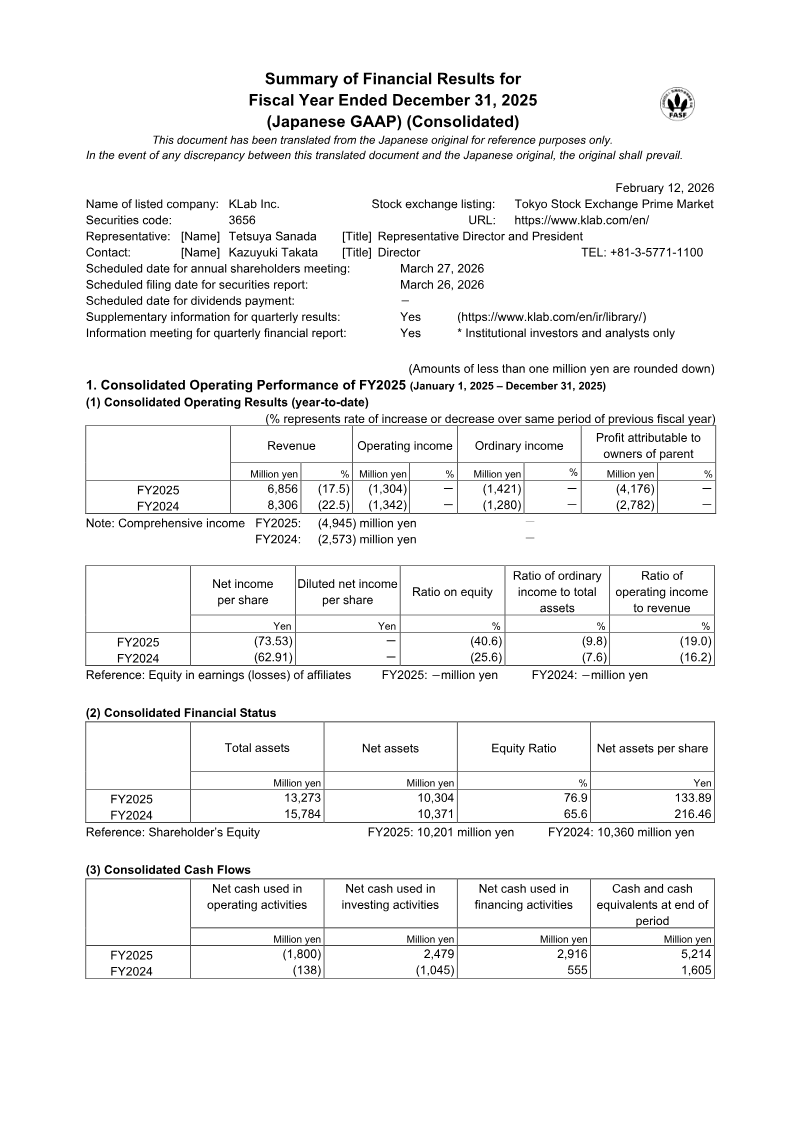

KLab · 2026

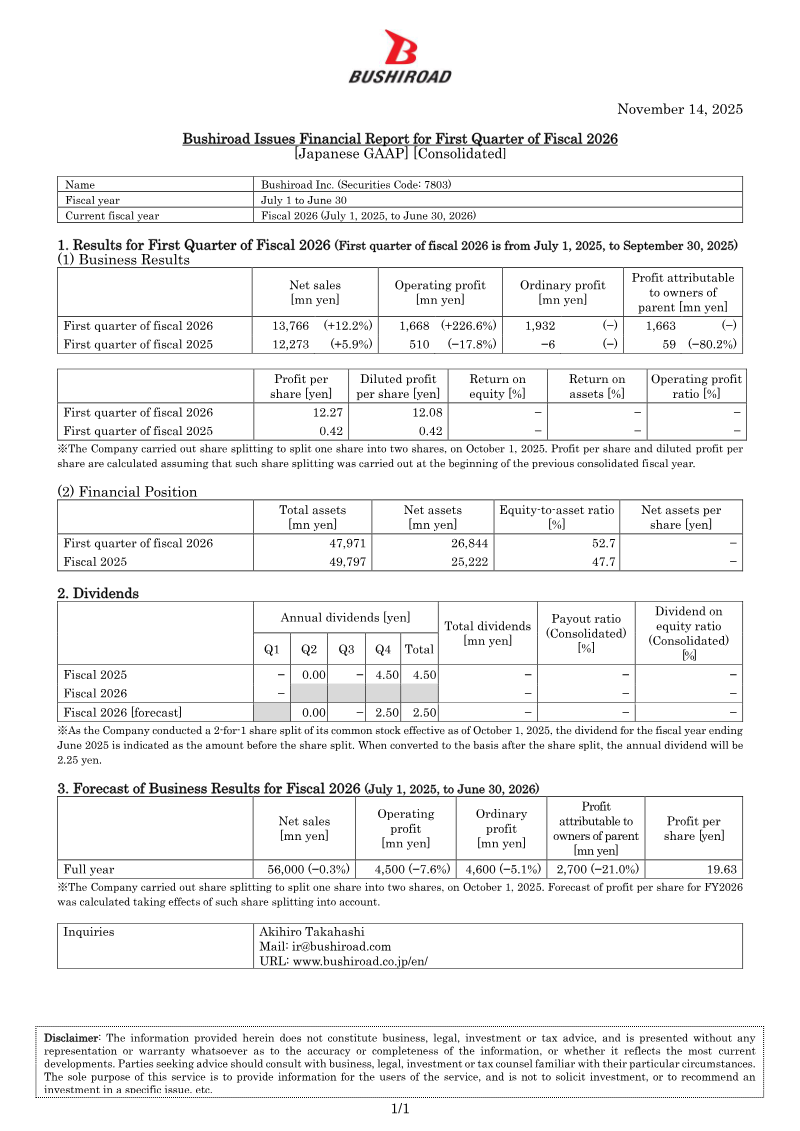

Bushiroad · 2025

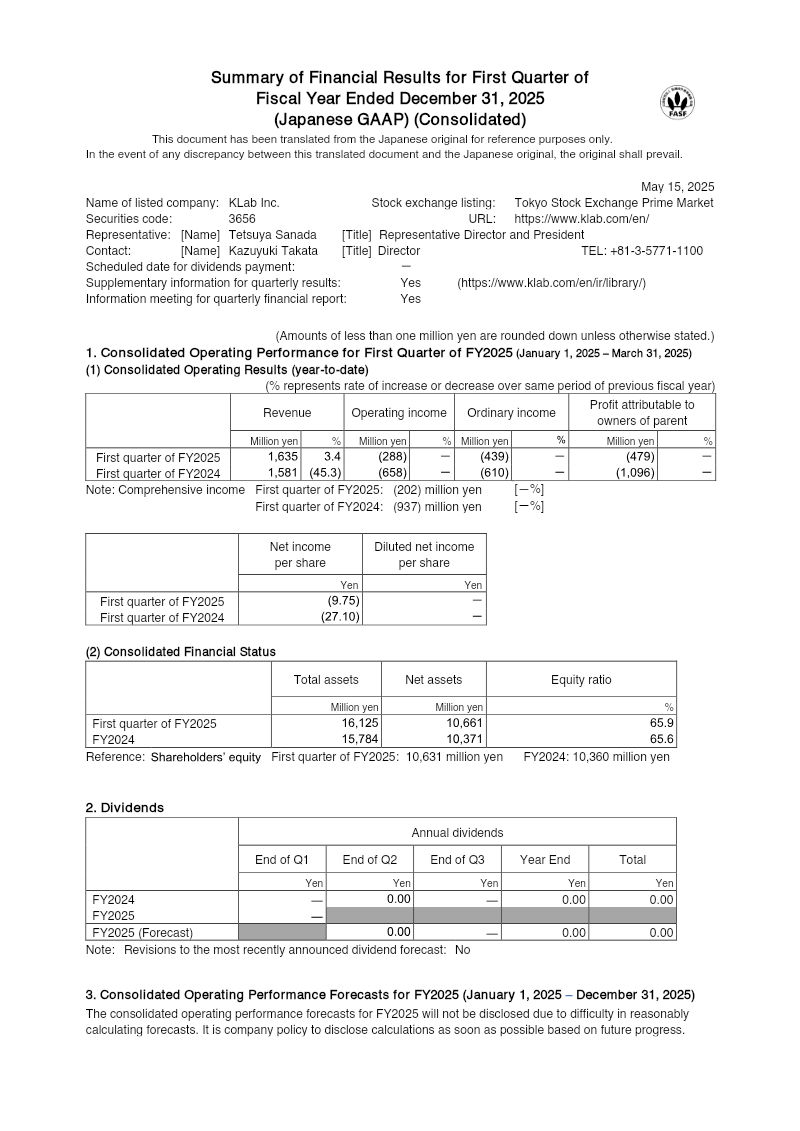

KLab · 2025

GREE · 2024

Bandai Namco · 2021

mixi · 2015

GREE · 2015

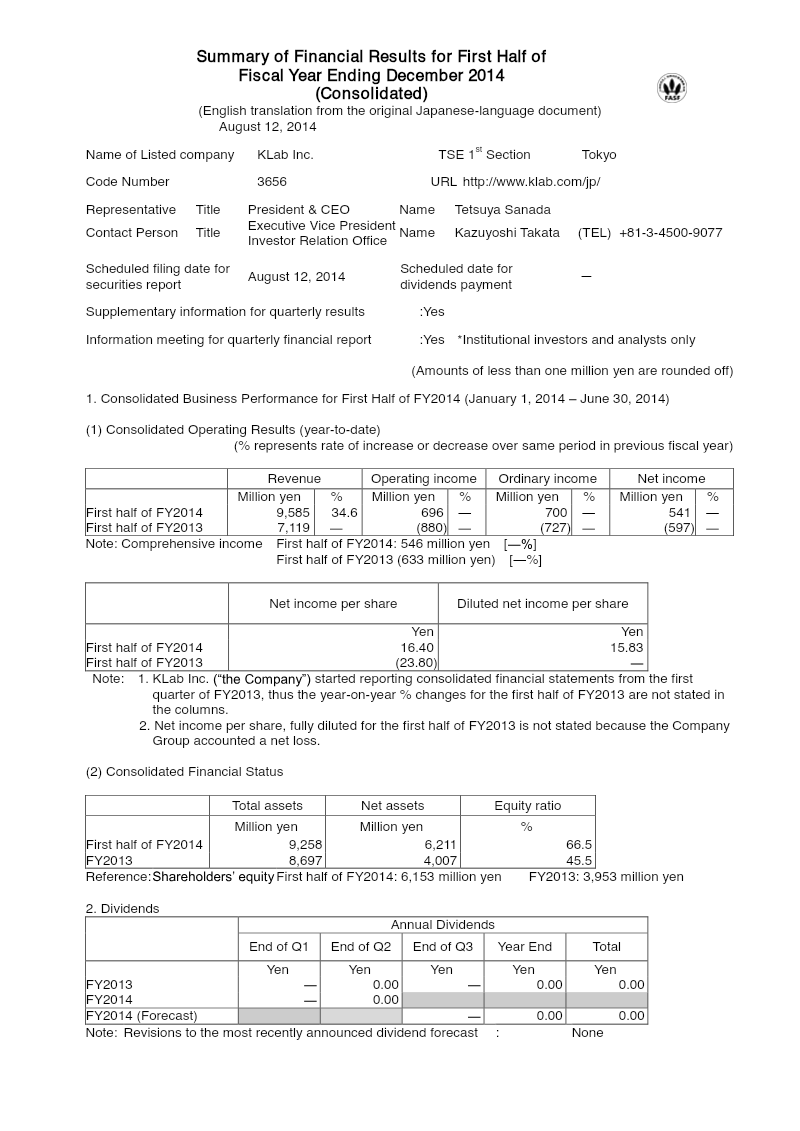

KLab · 2014

GREE · 2012

GREE

mixi