Report

Where the UGC Dollars Flow: Mapping $9B Investments in Creator Economy

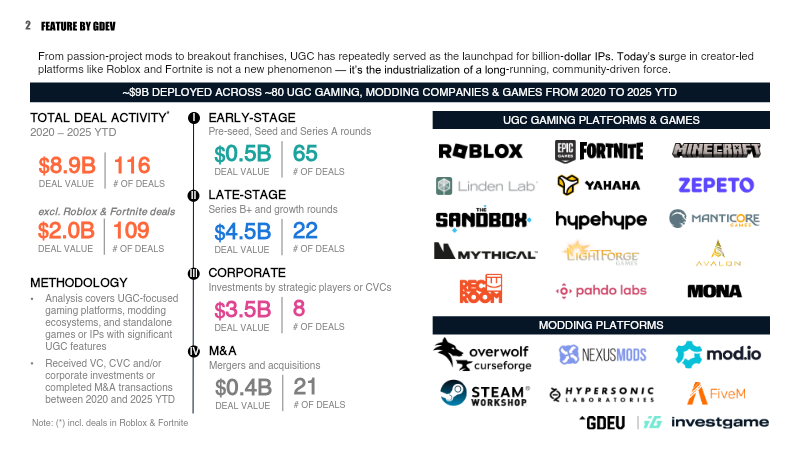

The analysis maps a $9 billion investment wave in user‑generated content (UGC) gaming from 2020 to 2025, covering roughly 80 companies and titles. Early‑stage rounds (pre‑seed to Series A) account for $0.5 billion, while late‑stage and corporate deals bring the total to $8.9 billion, including major platform names such as Roblox, Epic Games (Fortnite), Linden Lab, and Sandbox. Corporate venture capital and strategic investors contribute $3.5 billion, with notable commitments from Sony/Kirkbi ($2 billion in 2022) and Disney ($1.5 billion in 2024). Modding ecosystems—overwolf, mod.io, CurseForge—receive $0.4 billion in VC or M&A activity. The report tracks engagement metrics, noting Roblox’s 73.5 billion logged hours in 2024 and a peak concurrent user base of 21 million, while Fortnite Creative stabilizes around 1.3 million concurrent users. Creator payouts have risen sharply, with Roblox and Fortnite together disbursing approximately $1.5 billion to developers in 2024, and quarterly earnings showing a 38 % increase from Q2 23 to Q3 23. Funding follows a classic hype cycle: an initial surge during Roblox’s IPO and metaverse buzz (2020‑21), a pullback in 2022, and renewed strategic investment from incumbents in 2023‑24. Early‑stage rounds remain steady, averaging 12–15 deals per year, targeting “next Roblox/Fortnite” platforms and infrastructure. The largest early‑stage investments include $50 million raised by YAHAHA in 2020 and multiple $15–40 million Series A rounds for platforms such as ZAllbaba, Manticore, and Lighforge. Overall, the data illustrate a mature UGC ecosystem that has evolved from hobbyist modding to professionalized creator economies, with sustained capital inflows and growing monetization pathways for both platforms and individual creators.

InvestGame

Report

Fashion & Beauty Trends: How Gen Z Express Themselves in Immersive Spaces 2023

The 2023 analysis of digital expression among Generation Z demonstrates that immersive platforms have become the primary arena for personal style and identity formation. Across the year, more than half of Gen Z respondents now prioritize styling their avatars over physical clothing, and a substantial majority regard digital fashion as at least somewhat important, with over half noting a marked increase in relevance since the previous year. This shift is reflected in a 38 percent rise in avatar updates, reaching 165 billion actions, and a 15 percent growth in the purchase of virtual fashion items, totaling 1.6 billion transactions. Monthly spending on digital looks clusters between ten and one hundred dollars, driven especially by limited‑edition pieces that command significant resale premiums. Customization behavior reveals a strong focus on clothing and hair, each selected by roughly half of users, while a sizable portion aligns skin tone and body type with their real‑world appearance. Daily or weekly avatar adjustments are reported by 70 percent of participants, with female‑identifying and non‑binary players leading the trend. Hairstyle purchases alone surged 20 percent to exceed 139 million items, underscoring the depth of aesthetic investment. Beyond consumption, Gen Z leverages these spaces for co‑creation and personal development. Collaborative projects such as a Fenty Beauty product that amassed over one million community votes and student‑driven translations of digital runway concepts into physical garments illustrate the platform’s role as an incubator for fashion innovation. Moreover, 88 percent of respondents claim virtual self‑expression enhances their offline identity, while notable percentages report improved social connections, mood, and confidence, suggesting tangible mental‑health benefits. Industry forecasts anticipate that leading fashion talent will increasingly emerge from these immersive environments, positioning digital platforms as pivotal to the future of fashion and beauty.

RobloxJan 2023