Japan

Report

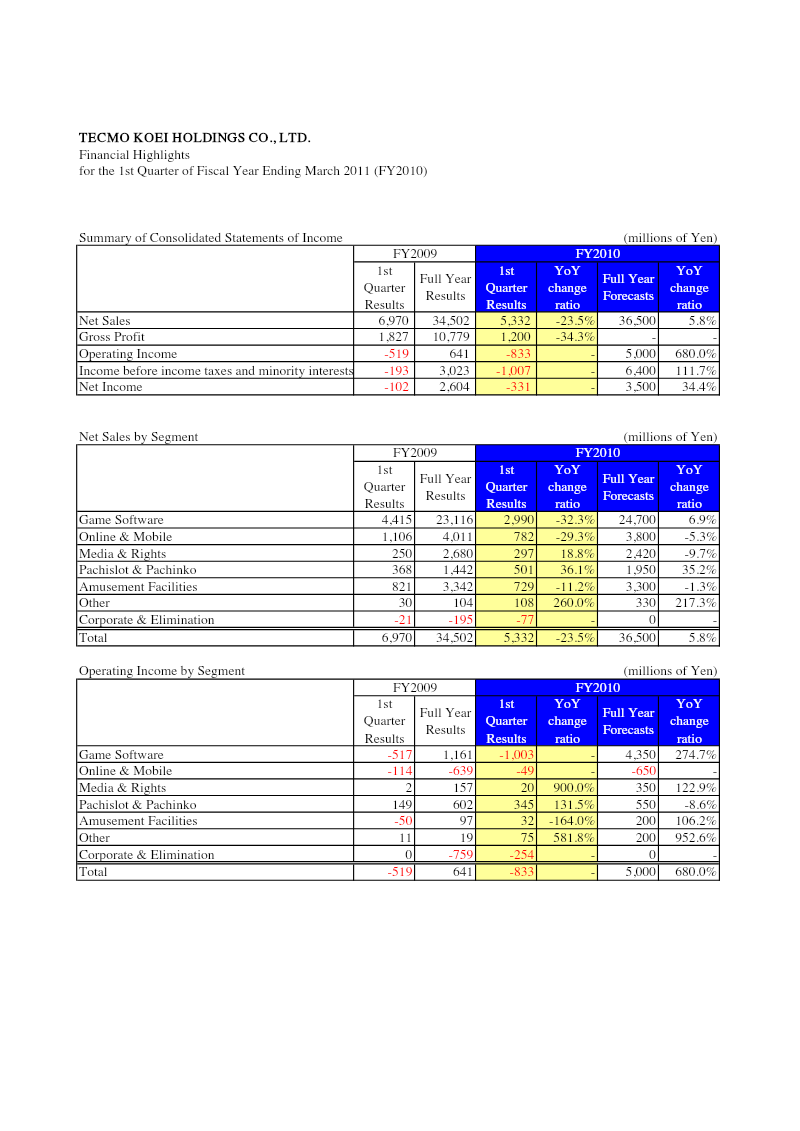

Financial Highlights: 1st Quarter of Fiscal Year Ending March 2011

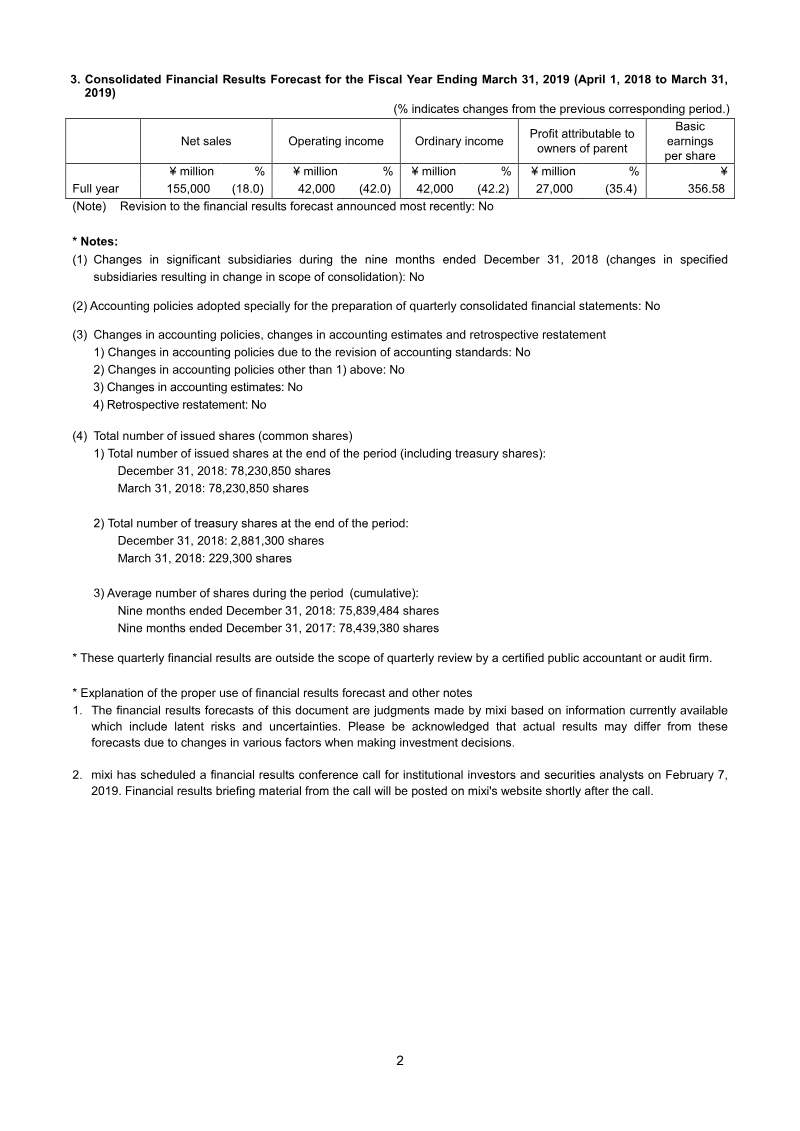

The financial highlights for the first quarter of fiscal year ending March 2011 reveal a mixed performance across Tecmo Koei Holdings’ operating segments. Net sales fell 23.5 % year‑over‑year to ¥34,502 million, driven mainly by declines in game software sales (−32.3 %) and online & mobile revenue (−29.3 %). In contrast, pachislot & pachinko sales rose 36.1 % to ¥1,442 million, while media & rights and amusement facilities experienced modest growth of 18.8 % and −11.2 %, respectively. The “Other” segment saw a sharp increase of 260 % to ¥104 million, though its absolute contribution remained small. Operating income swung from a loss of ¥519 million in the same quarter of FY2009 to a profit of ¥641 million, an improvement of 1,160 million yen. This turnaround was largely attributable to game software operating income rising from a loss of ¥517 million to a profit of ¥1,161 million. Online & mobile income improved from a loss of ¥114 million to a profit of ¥639 million, while media & rights and pachislot & pachinko also posted gains. The “Other” segment’s operating income increased markedly, though its impact on total profitability was limited by the overall scale. Net income shifted from a loss of ¥102 million to a profit of ¥2,604 million, reflecting the combined effect of stronger operating results and favorable tax treatment. Forecasts for the full year project net sales growth to 5.8 % and operating income to 680 %, indicating management’s expectation of a rebound in game software sales and continued strength in pachislot & pachinko. The analysis covers all business units within the company, with data expressed in millions of yen for FY2009 and FY2010, and includes year‑over‑year comparisons and forecasted full‑year figures.

Koei Tecmo

Report

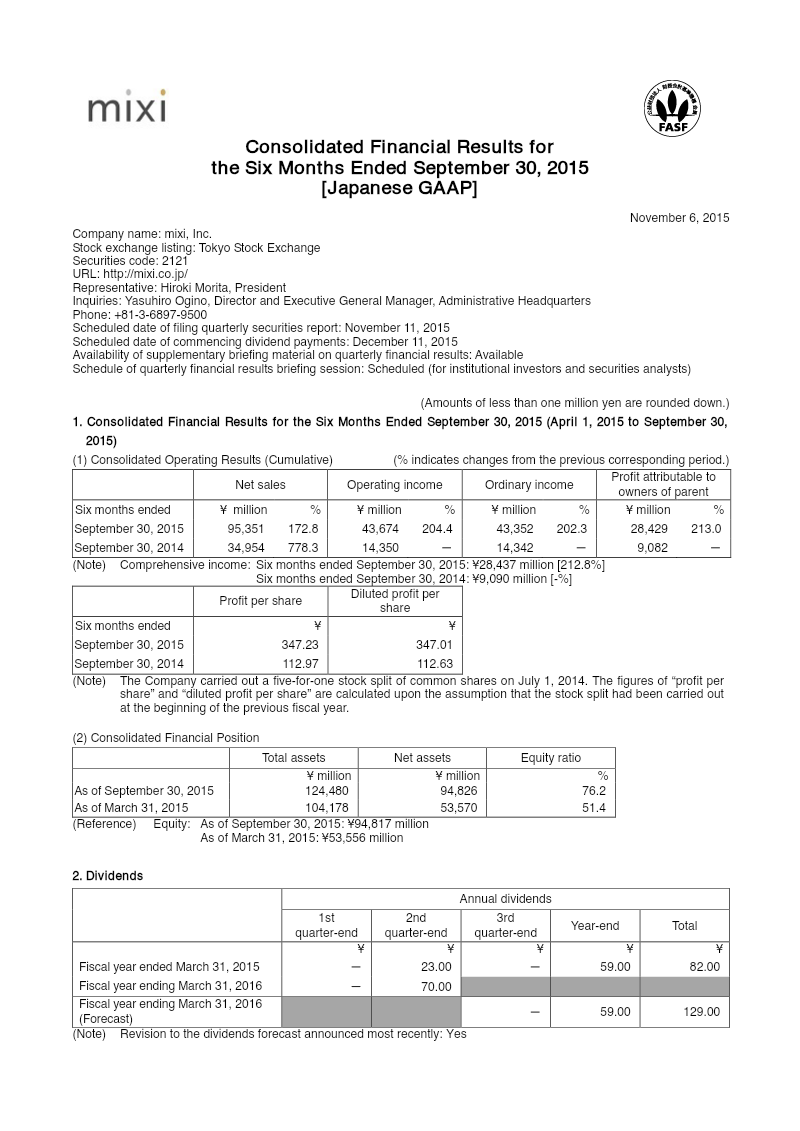

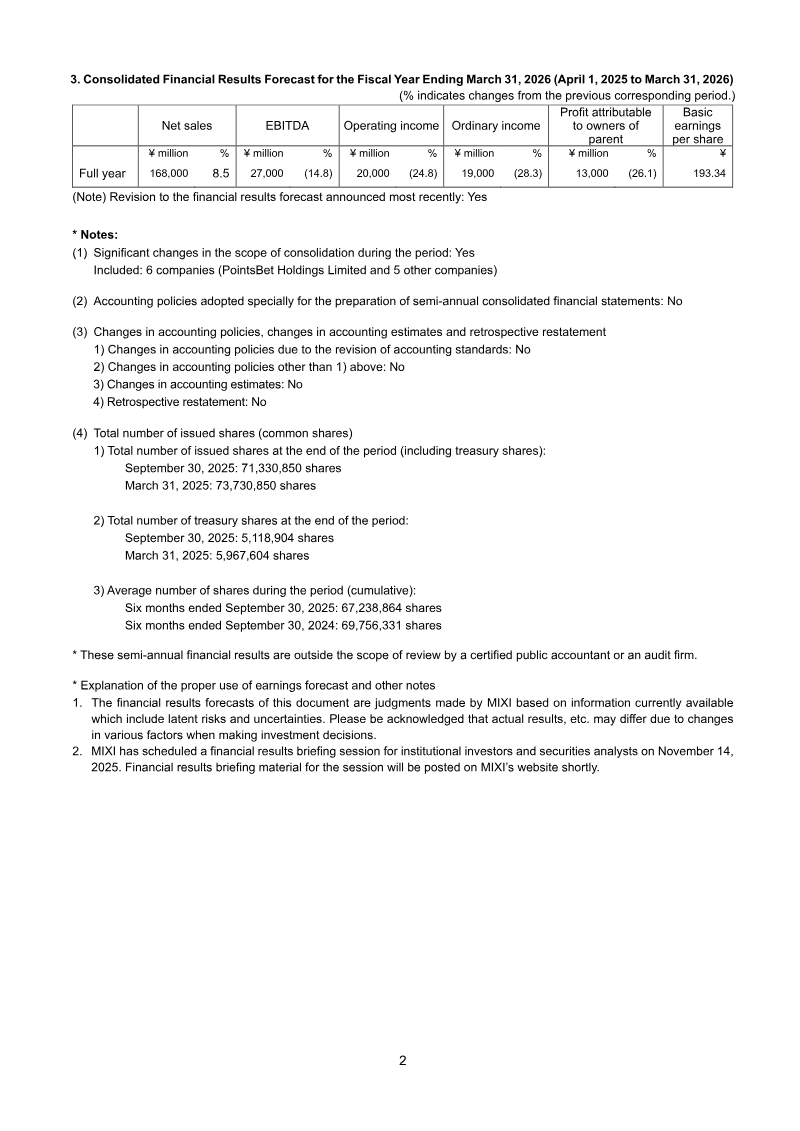

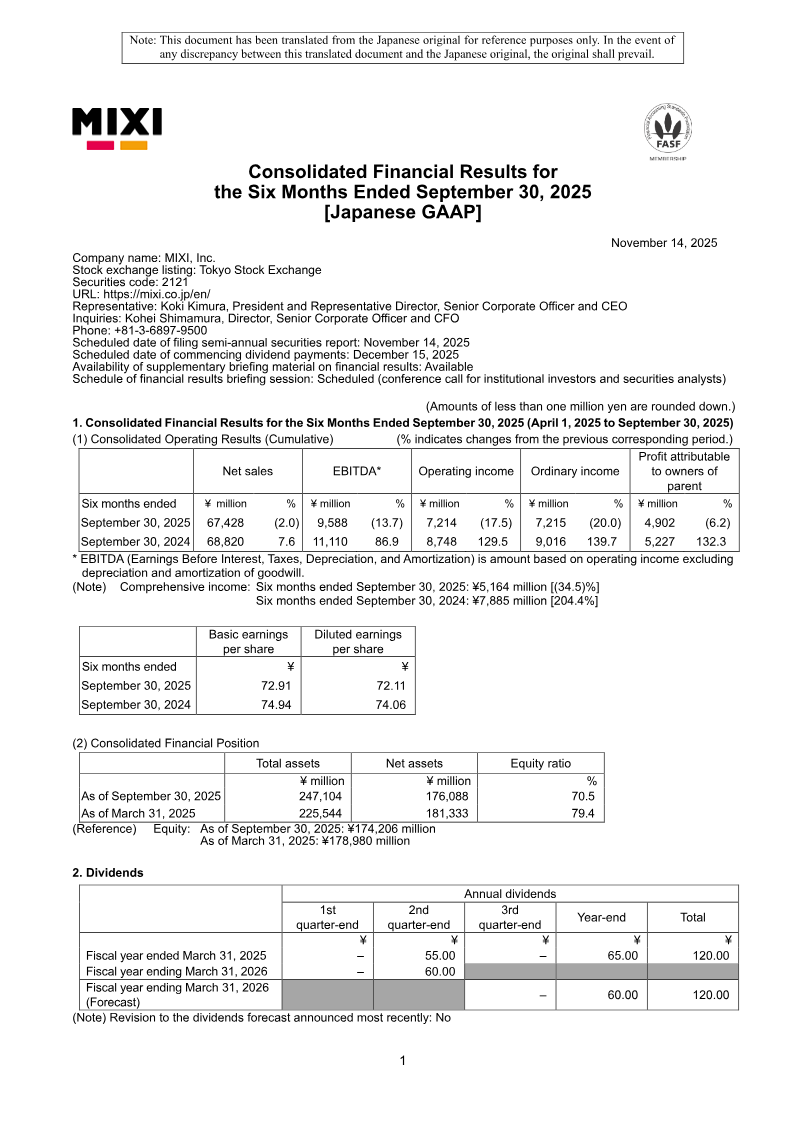

Consolidated Financial Results for the Six Months Ended September 30, 2025: Japan

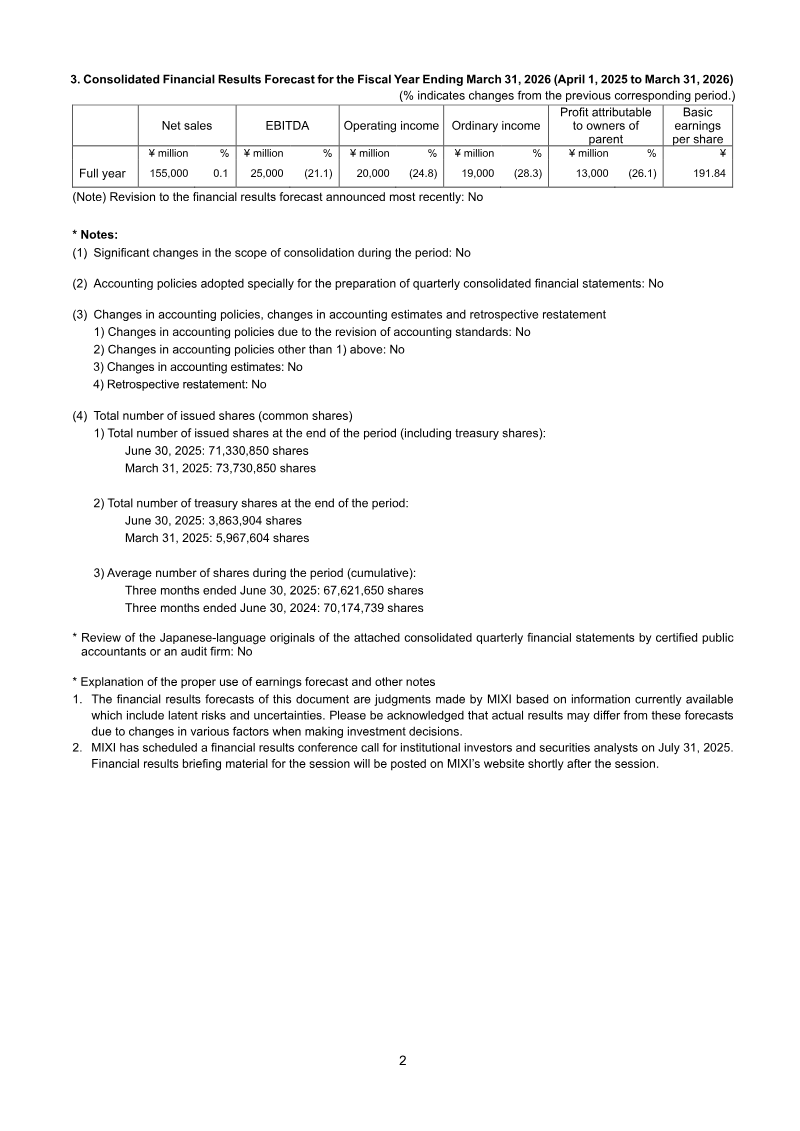

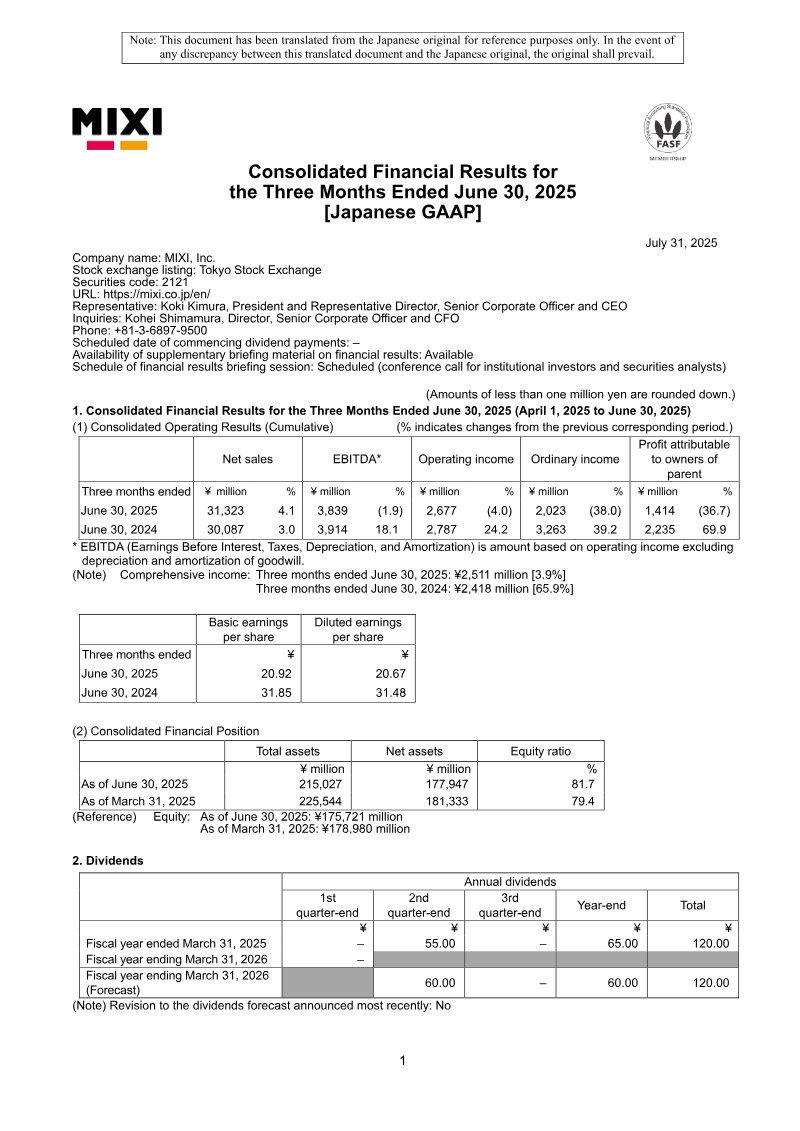

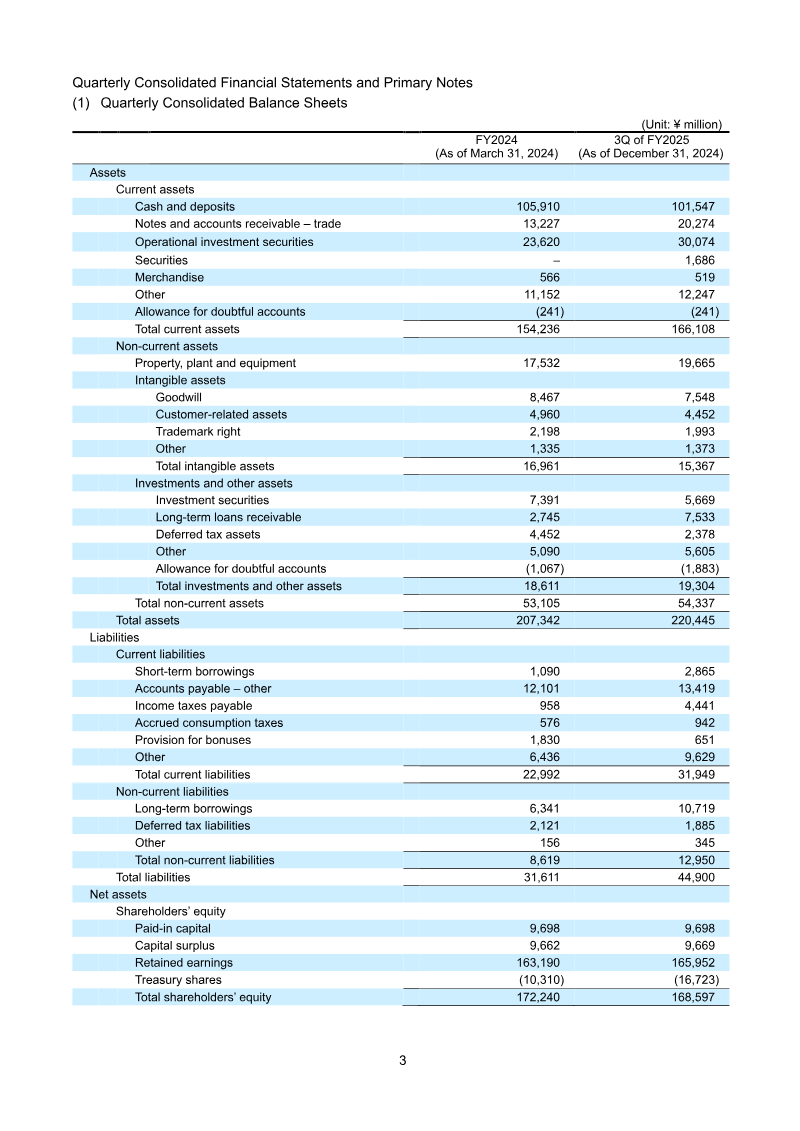

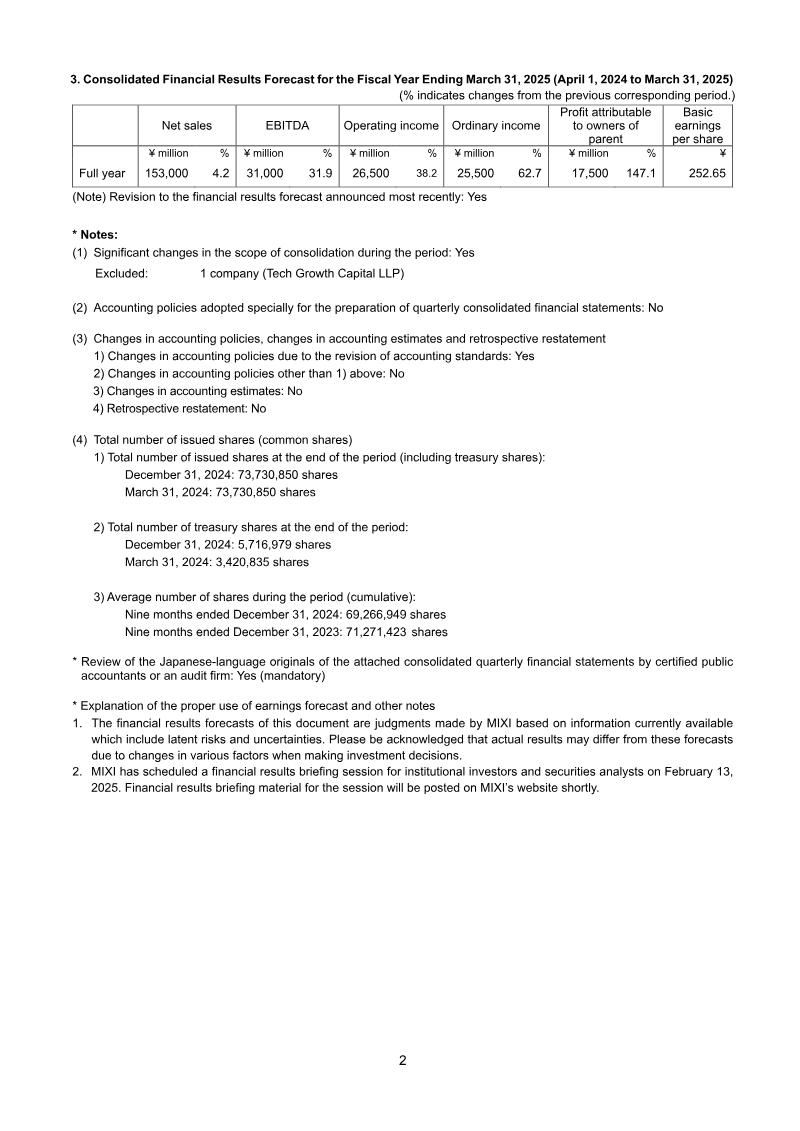

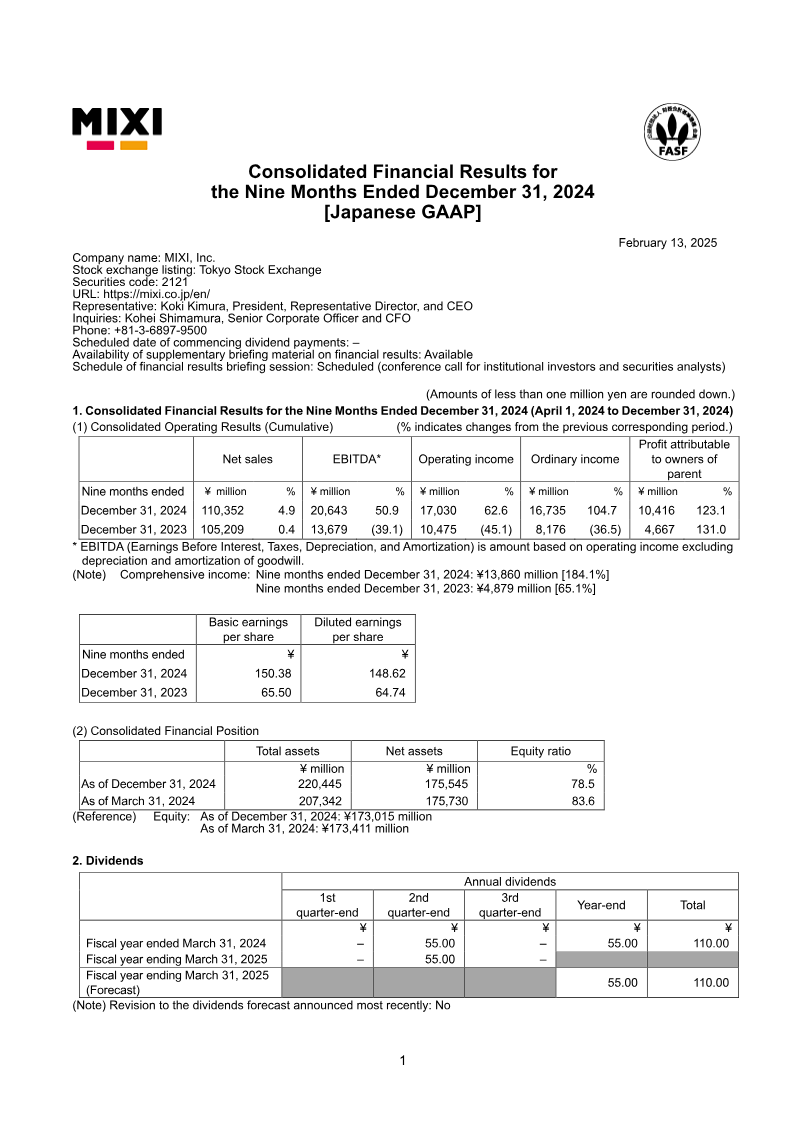

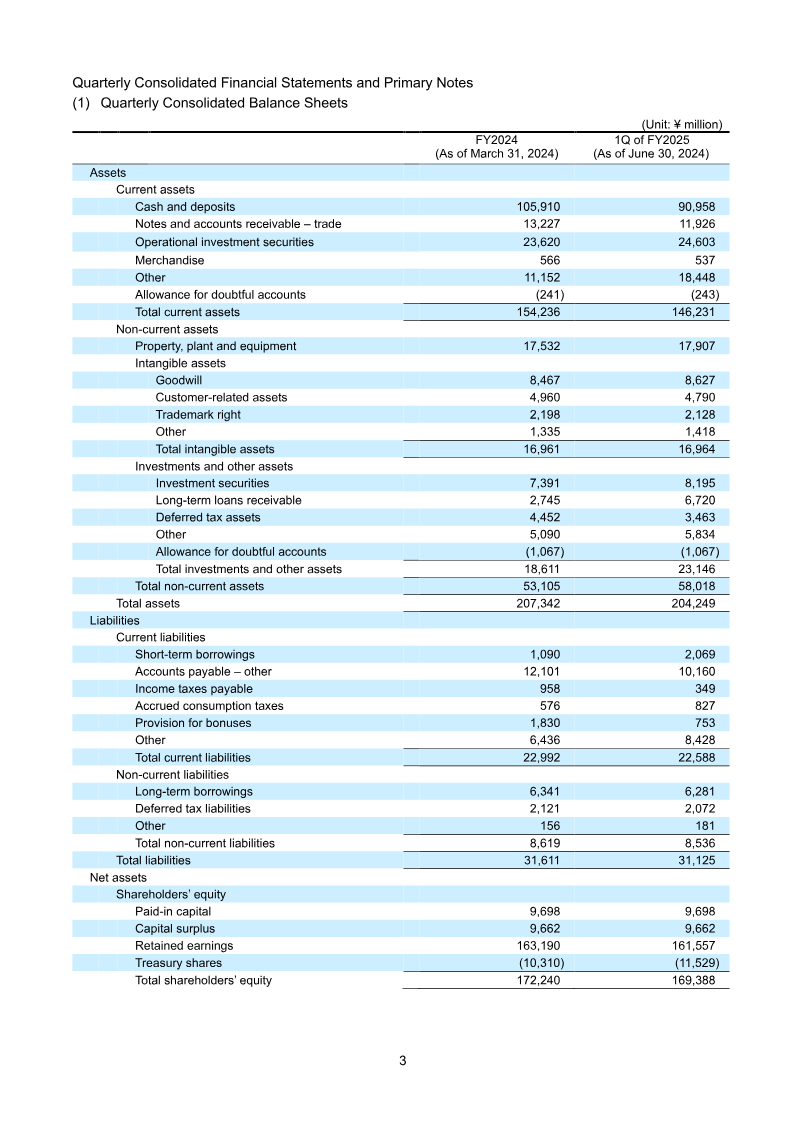

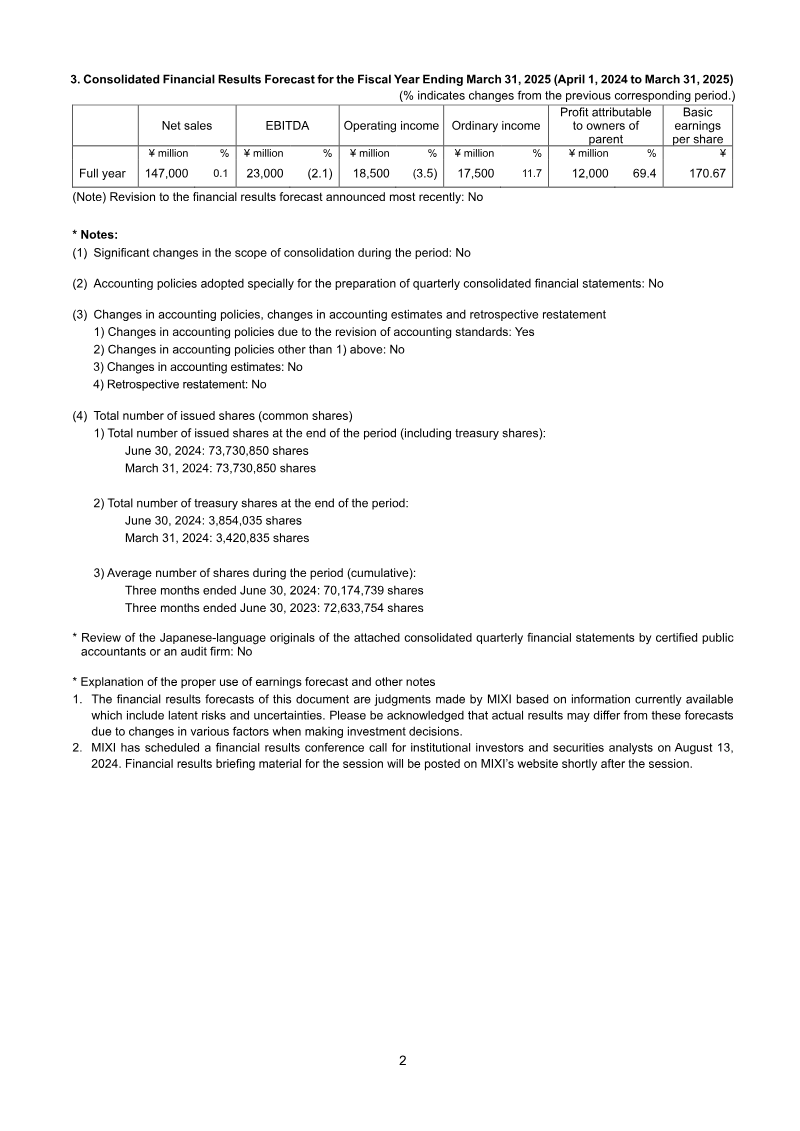

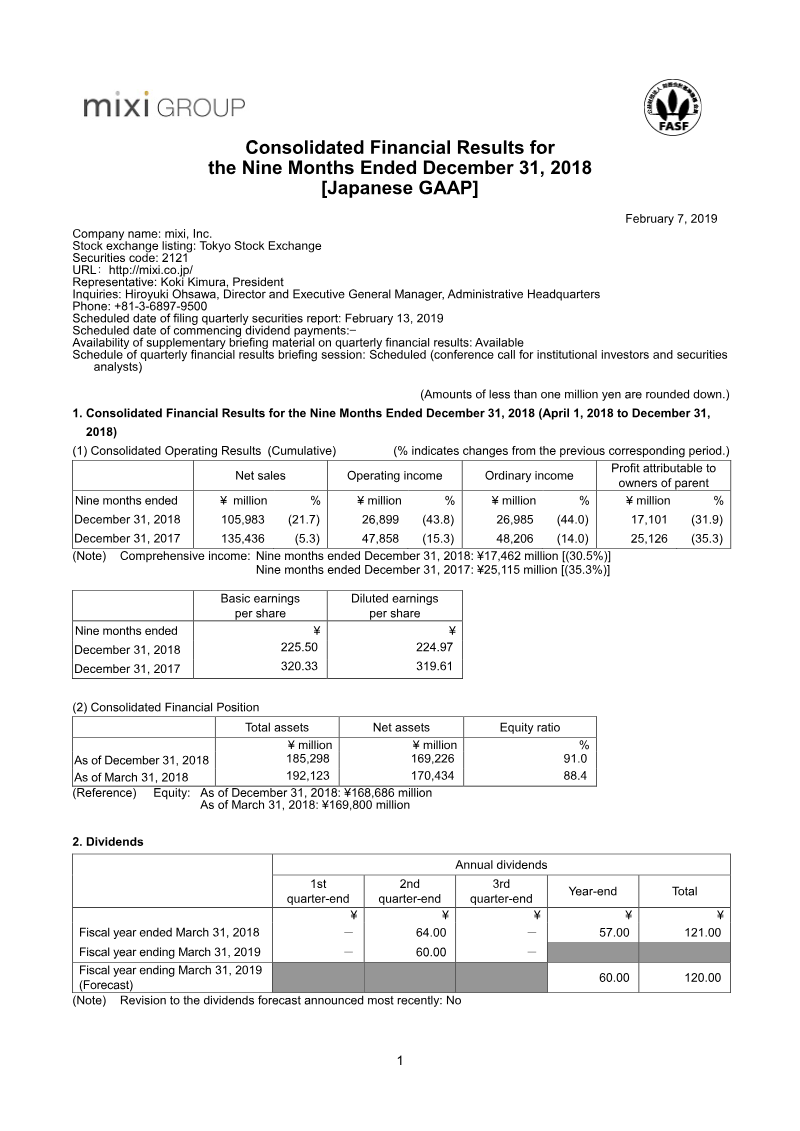

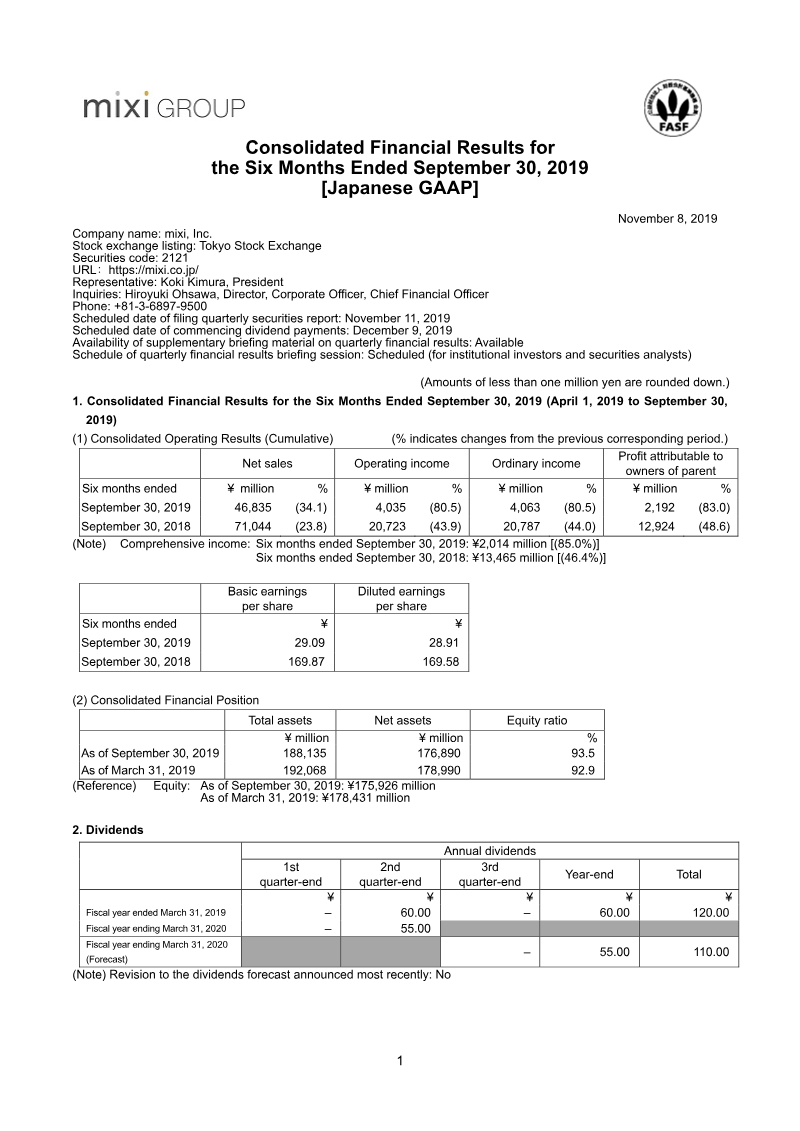

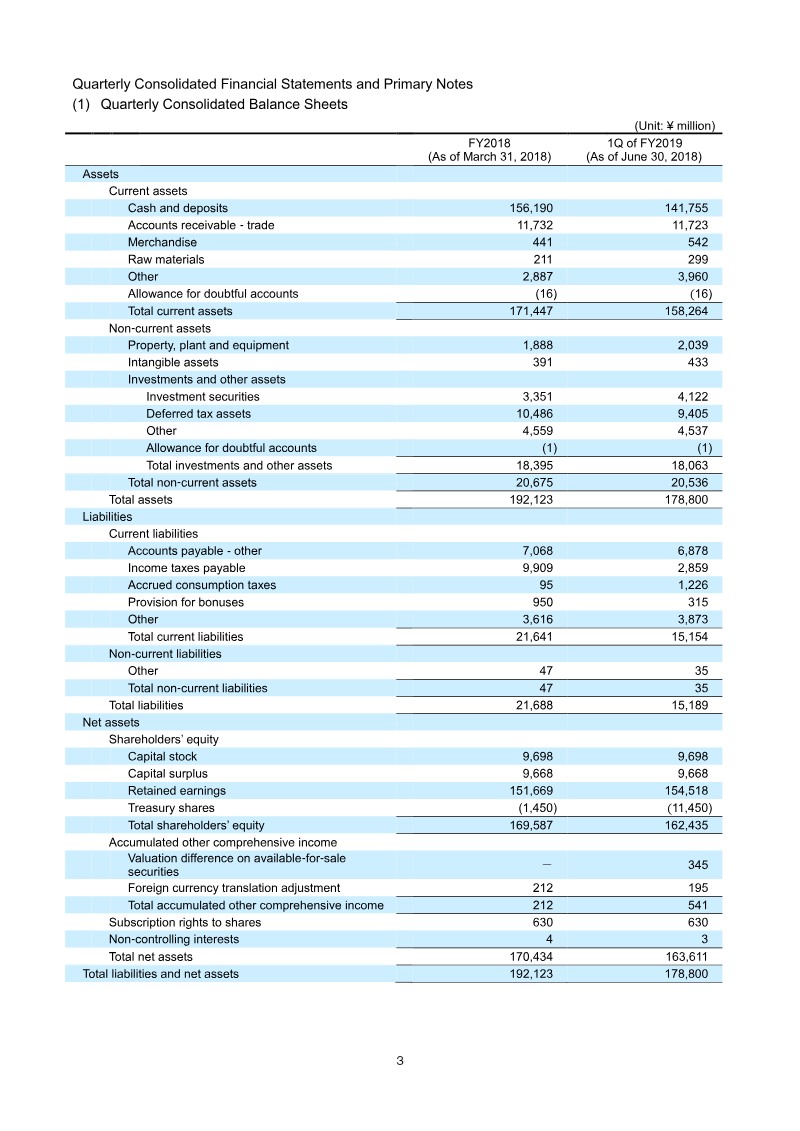

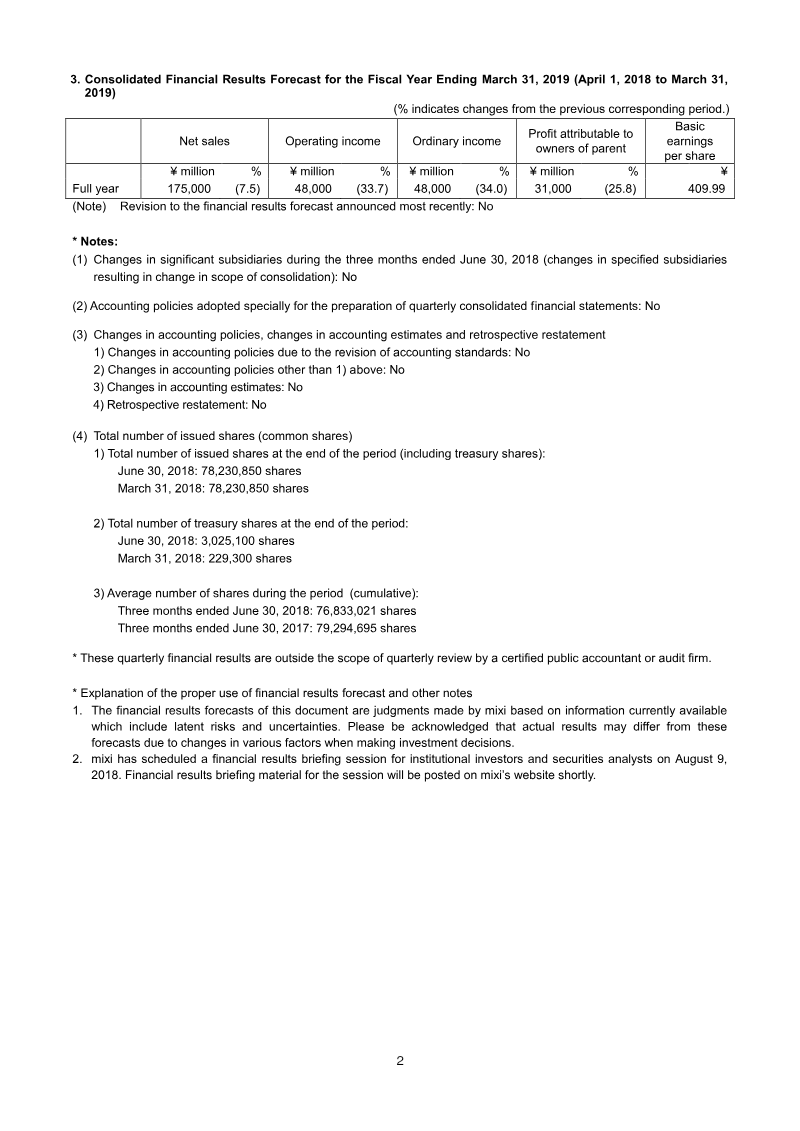

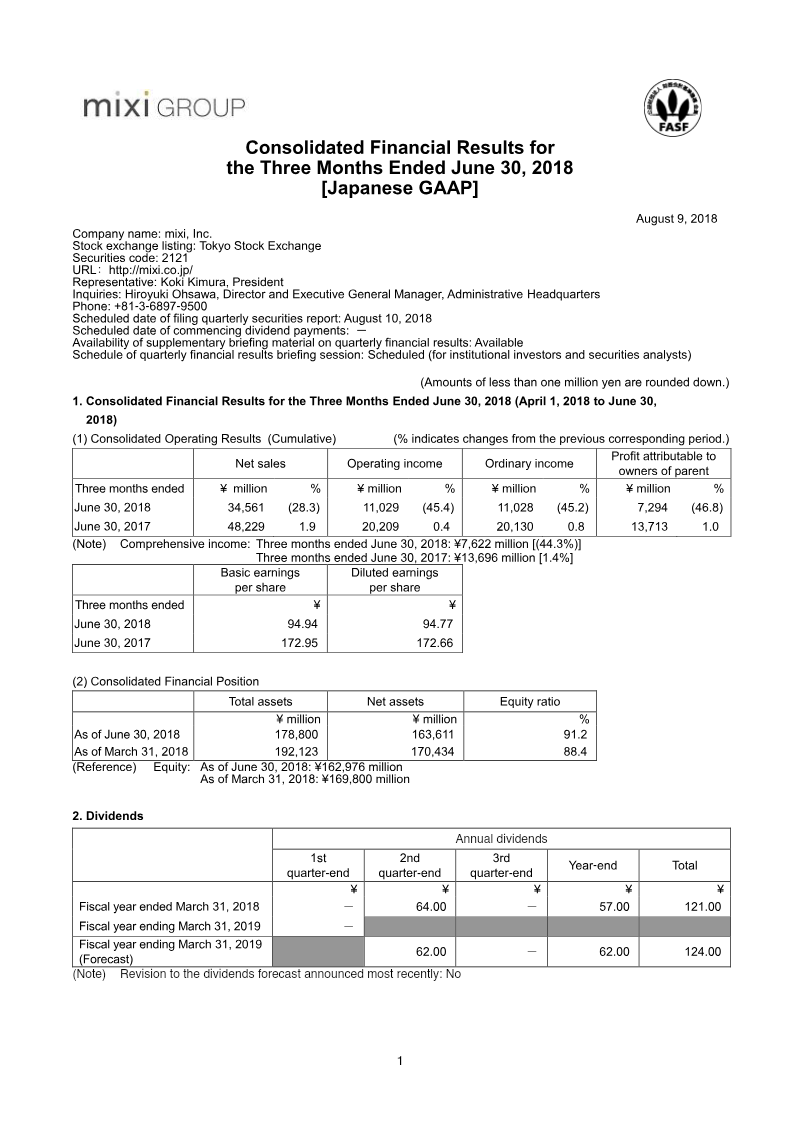

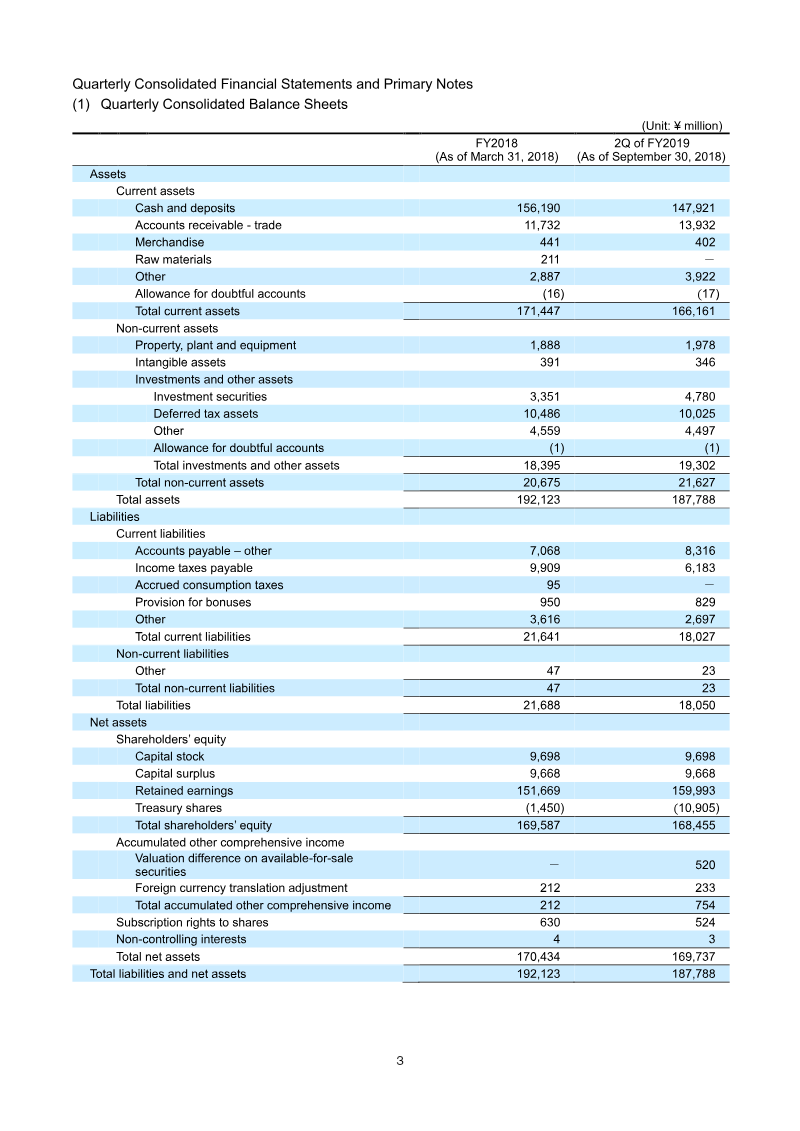

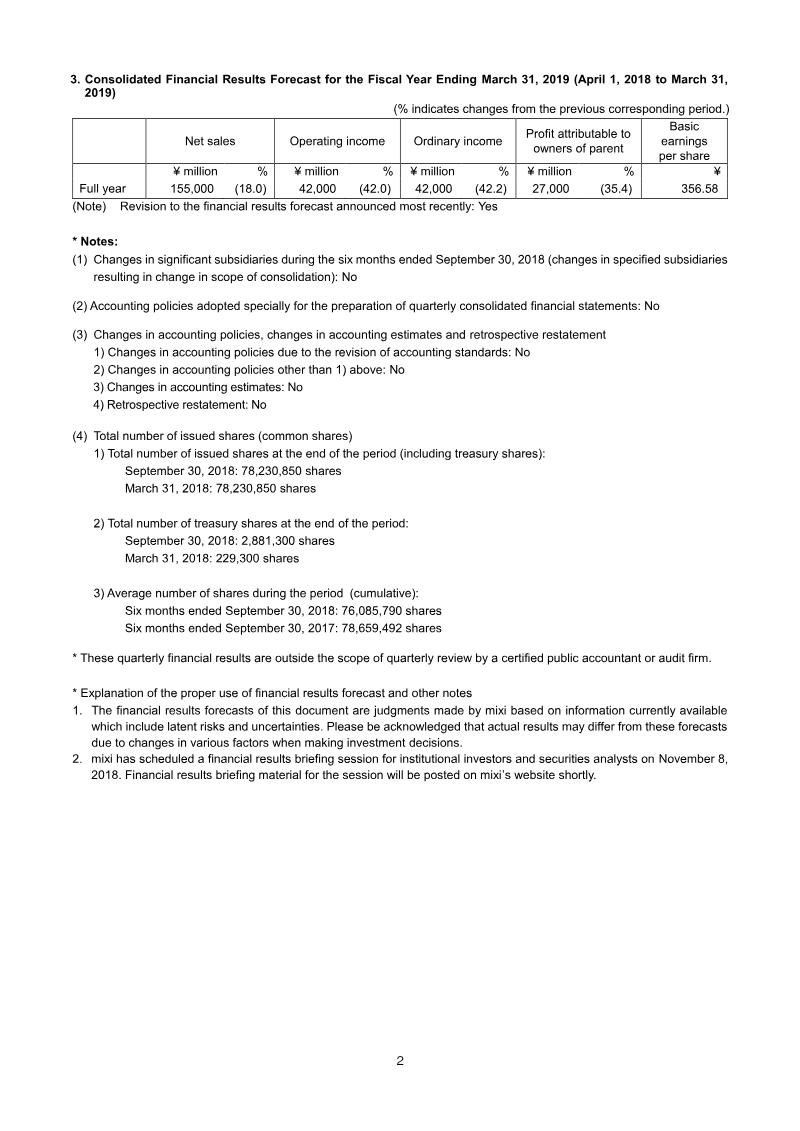

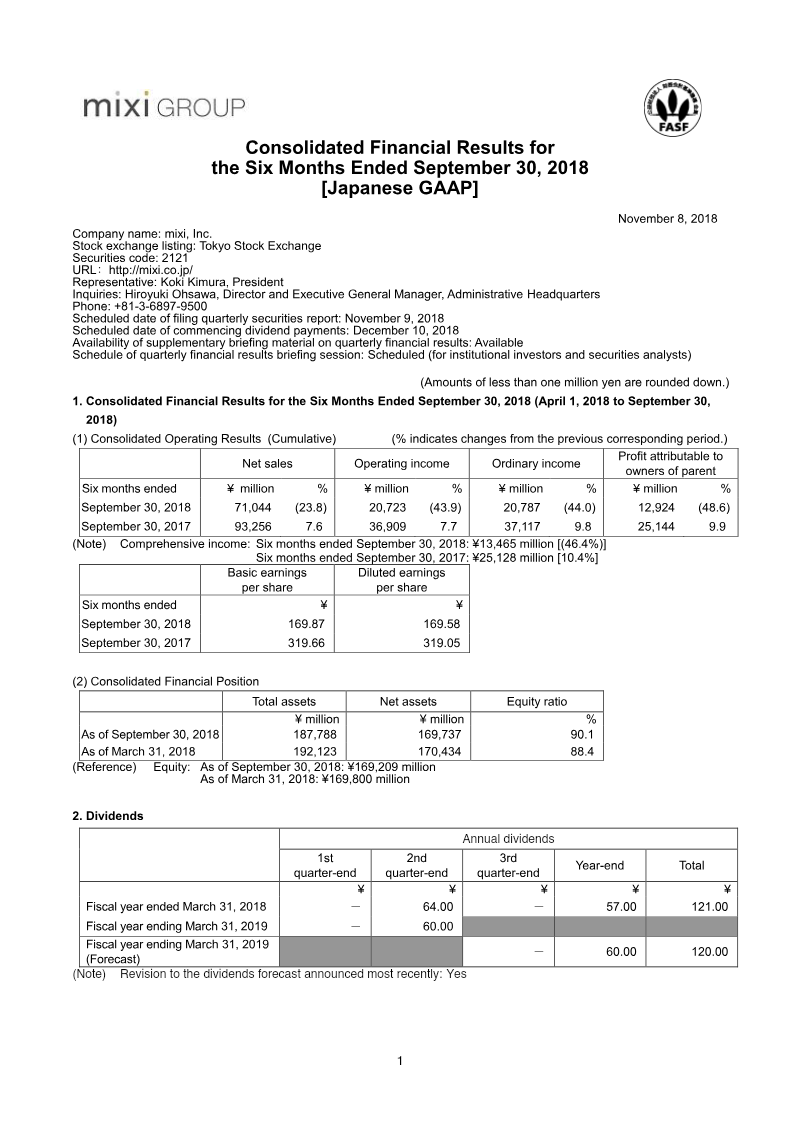

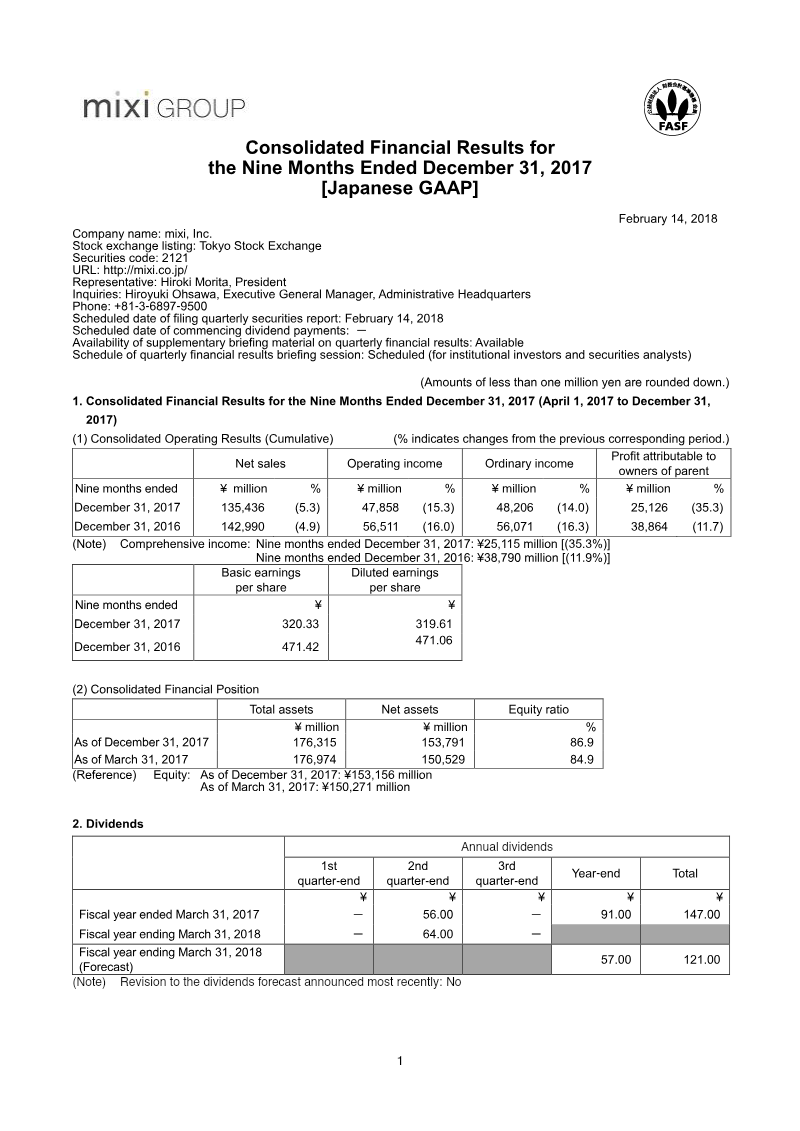

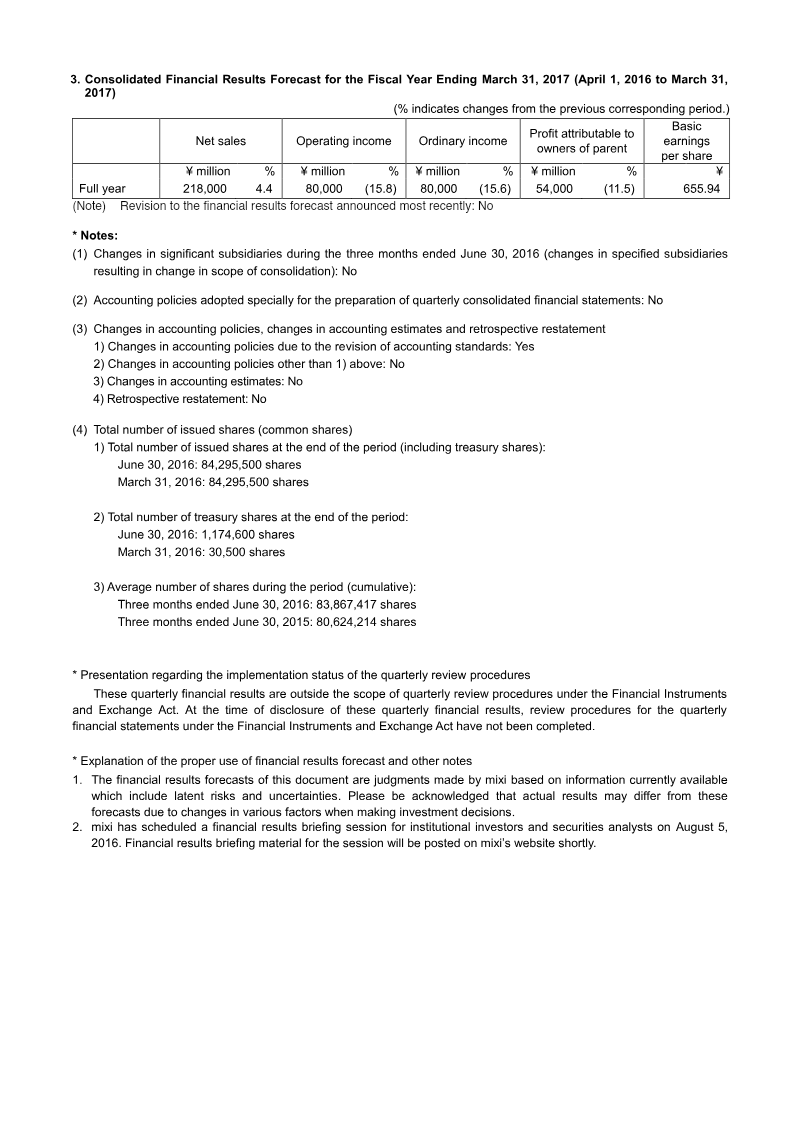

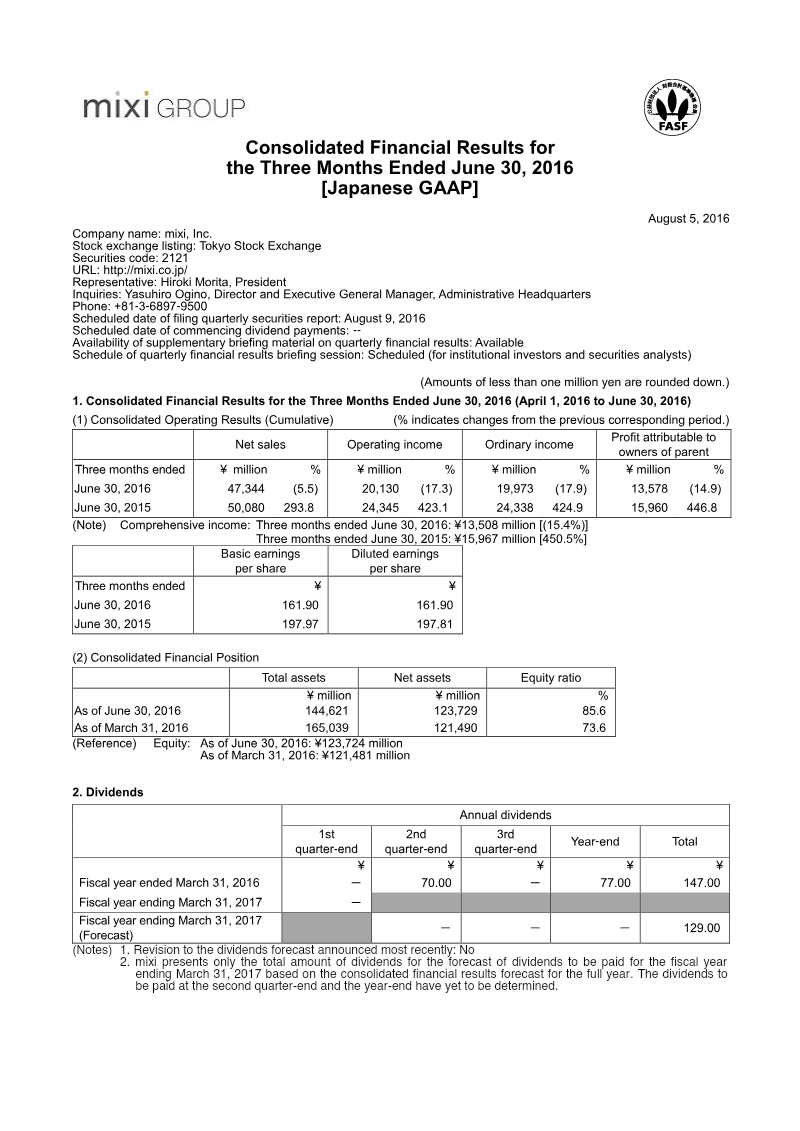

MIXI, Inc. reports consolidated financial results for the six months ended September 30 2025 under Japanese GAAP, covering April 1–September 30. Net sales declined 2.0 % YoY to ¥67,428 million, with EBITDA falling 13.7 % to ¥9,588 million and operating income dropping 17.5 % to ¥7,214 million. Ordinary income to owners of parent decreased 20.0 % to ¥7,215 million, and profit attributable to owners of parent fell 6.2 % to ¥4,902 million. Comprehensive income for the period was ¥5,164 million, a 34.5 % decline from ¥7,885 million the prior year. Segment performance varied: Digital Entertainment revenue fell 11.1 % to ¥35,692 million but segment profit rose 2.5 % to ¥16,571 million due to cost efficiencies; Sports Business sales increased 20.5 % to ¥21,977 million but segment profit fell 38.6 % to ¥441 million after acquisition‑related expenses; Lifestyle Business sales grew 30.0 % to ¥7,094 million, turning a prior loss into a ¥72 million profit; Investment Business sales declined 46.8 % to ¥2,637 million and profit fell 39.1 % to ¥1,465 million. Total assets rose to ¥247,104 million, with net assets at ¥176,088 million and an equity ratio of 70.5 %. Cash and cash equivalents fell ¥22,883 million to ¥85,290 million, driven by operating cash outflows and significant investing cash used for a subsidiary acquisition that added ¥25,533 million of goodwill. Short‑term borrowings increased sharply to ¥21,175 million. The company revised its full‑year forecast for FY2026, lowering net sales to ¥168 billion and EBITDA to ¥27 billion. Dividend policy remains unchanged, with a total annual dividend of ¥120 million for FY2025 and a forecast of ¥120 million for FY2026. The report includes detailed segment disclosures, goodwill changes from the PointsBet acquisition, and treasury‑share activity affecting equity.

mixi