Related Documents

Financial

Games Investment Review: Q2 2023

In the second quarter of 2023, the games industry attracted $425.7 million in capital across 92 completed transactions, marking a modest rise from the previous quarter. The influx of funding underscores a continued appetite for growth within the sector, despite broader market volatility, and suggests that investors remain confident in the commercial prospects of interactive entertainment. The analysis focuses exclusively on deals that have reached closing, deliberately omitting announced but unfinalized transactions. This approach, applied consistently for fourteen years, aims to capture actual money deployed rather than projected activity. For special‑purpose acquisition companies, the reported figures represent the amount of capital raised in the transaction, not the post‑deal enterprise valuation, which distinguishes the data set from many alternative sources that may inflate quarterly totals by including speculative valuations. By adhering to this stringent methodology, the review provides a more dependable benchmark for stakeholders monitoring genuine investment and acquisition trends in the games sector. The resulting figures, while sometimes divergent from other reports, offer a clearer picture of real financial commitment and enable more accurate forecasting of industry dynamics. Overall, the quarter’s investment performance signals steady, if measured, confidence in the sector’s capacity to generate returns and sustain expansion.

DDMJun 2023

Financial

Games Investment Review Q4 2023 Executive Summary Report

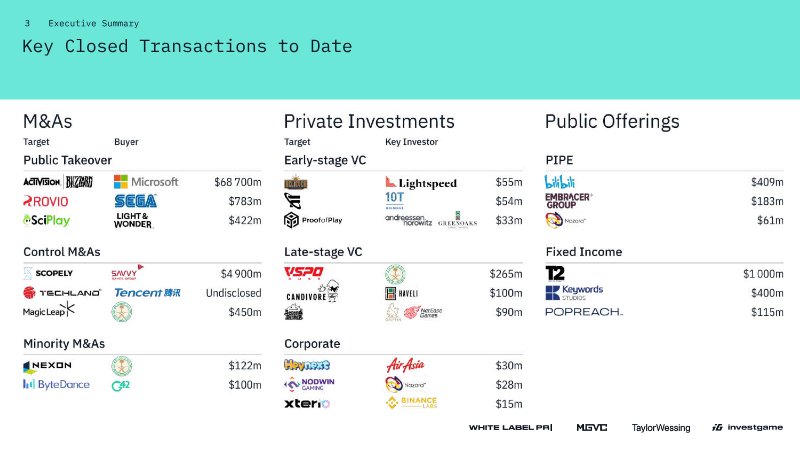

The analysis evaluates global capital flows into the video‑games ecosystem throughout 2023, with a focus on the fourth quarter, to gauge how mega‑transactions and shifting investor priorities are reshaping the market. The central thesis is that headline‑grabbing acquisitions mask a broader contraction in deal activity, prompting a more disciplined allocation of funds as the sector confronts macro‑economic pressures and tighter regulatory environments, particularly in China. Overall M&A volume fell 22 % year‑on‑year, yet Q4 recorded a record $70.8 bn in total deal value, 98 % of which derived from Microsoft’s $68.7 bn purchase of Activision Blizzard. Excluding that outlier, annual M&A would have amounted to just $11.4 bn, an 80 % decline. Private‑equity and venture investment also weakened, with Q4 investment volume dropping to $936.6 m—the first sub‑$1 bn quarter since 2018—and the number of deals falling 21 %. IPO activity remained flat at three offerings, though market‑cap surged 257 % to $112 m. AI‑related funding accounted for 28 % of undisclosed deals, totaling $319 m across 61 transactions, while blockchain financing collapsed 72 % in value to $1.4 bn despite a modest revival after the SEC approved spot‑bitcoin ETFs. Geographically, Europe dominated the quarter with roughly $308 m across 20 deals, Asia trailed, and the remainder of the world contributed about 12 % of undisclosed volume. Sovereign wealth funds entered the arena more prominently, exemplified by Saudi Arabia’s $4.9 bn acquisition of Scopely and a $265 m stake in e‑sports firm VSPO. The outlook for 2024 anticipates continued headwinds and stricter Chinese regulation, but forecasts a stabilization of investment and IPO activity in the second half of the year as valuations soften and strategic capital deployment becomes the norm.

DDMDec 2023

Financial

Gaming Deals Report 2023 Q3: Glimpse of Normalization

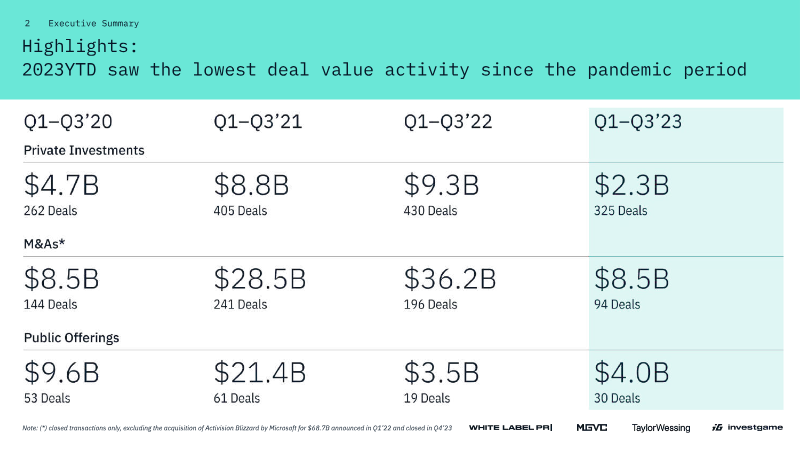

The analysis tracks closed financing and merger activity across the global video‑games sector through the first three quarters of 2023, comparing it with the pandemic‑era surge of 2020‑22. Its central thesis is that the market is entering a phase of normalization, with deal volumes and values falling to their lowest levels since the early‑pandemic period. Across all categories, total capital deployed in 2023 is markedly lower: private‑equity funding reached $2.3 billion, roughly one‑quarter of the $9.1 billion average recorded in 2021‑22, while the number of transactions dropped about 23 %. M&A activity contracted to $8.5 billion, a 3.8‑fold decline from the $36.2 billion average of the prior two years, and the bulk of that value was concentrated in a few marquee deals such as Microsoft’s $68.7 billion acquisition of Activision Blizzard and Scopely’s $4.9 billion sale to Savvy Games Group. Public‑market exits remained muted, with IPO and secondary offerings totaling $4.0 billion, far below the $21.4 billion raised in 2022. Early‑stage venture activity showed modest resilience; seed and pre‑seed rounds stayed near pre‑COVID levels, but large Series A deals fell sharply, with only five such transactions in Q1‑Q3 2023. Late‑stage financing was especially constrained, delivering just $300 million across eight rounds and prompting expectations of down‑rounds, premature exits, or bankruptcies for many firms that expanded during the boom years. Corporate investors shifted toward co‑investment with venture funds, particularly in Asia, while overall strategic‑investor participation declined across all regions. Geographically, North America accounted for $327 million of early‑stage venture capital, Western Europe $128 million, and Asia $85 million, with Eastern Europe, the Middle East‑North Africa, Africa, Latin America and Oceania contributing modest sums. AI‑focused gaming startups attracted heightened interest, closing 21 deals worth $268.1 million

InvestGameMar 2024

Financial

DDM Games Investment Review Q4 2023 Executive Summary Report

Digital Development Management (DDM) provides a comprehensive analysis of global video game investments, mergers and acquisitions (M&A), and initial public offerings (IPOs) for the full year and fourth quarter of 2023. The review utilizes proprietary data spanning 16 years to track capital flow across industry segments including Mobile, Console/PC, eSports, AR/VR, and blockchain. The central thesis identifies 2023 as a year of "masked challenges." While the industry reached a record-breaking $81.1 billion in total transaction value, this figure was heavily skewed by Microsoft’s $68.7 billion acquisition of Activision Blizzard, which accounted for 85% of the year's total value. Excluding this outlier, M&A activity hit its lowest value since 2020, totaling only $8.0 billion. Similarly, pure investments fell to $4.4 billion across 616 deals, a 69% decline in value from 2022 and the lowest level since 2016. This contraction reflects a "corrective year" following pandemic-era highs, characterized by high-interest rates, macroeconomic headwinds, and a shift toward corporate restructuring and layoffs. Key findings highlight a "winter" in both eSports and blockchain. Blockchain investments dropped 72% in value year-over-year, while eSports saw significantly lower valuations, exemplified by FaZe Clan’s $17 million acquisition following a previous $725 million valuation. Conversely, Artificial Intelligence emerged as a growing interest area, securing $319 million across 61 investments. Geographically, Poland maintained its status as a global IPO hub, while Saudi Arabia’s Public Investment Fund signaled long-term disruption with major acquisitions like Scopely for $4.9 billion. The outlook for 2024 suggests continued volatility and "unprecedented layoffs" as companies divest non-core assets. However, DDM anticipates a stabilization in the latter half of the year as valuations bottom out, potentially triggering a wave of bargain-driven M&A activity. Methodology is strictly limited to closed transactions to ensure data consistency and accuracy.

Digital Development ManagementJan 2023