FinancialNintendo

Financial Results Explanatory Material: 3rd Quarter of Fiscal Year Ending March 2025

1 Feb 202525 pages~14 min full read

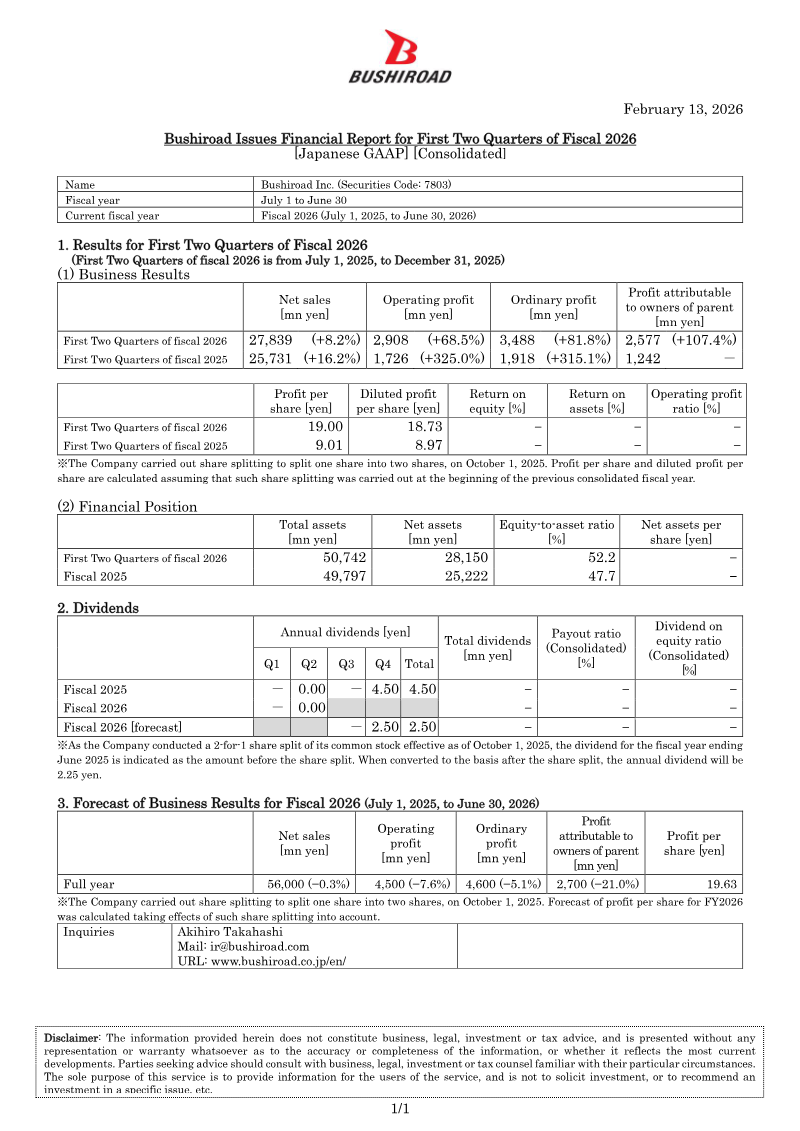

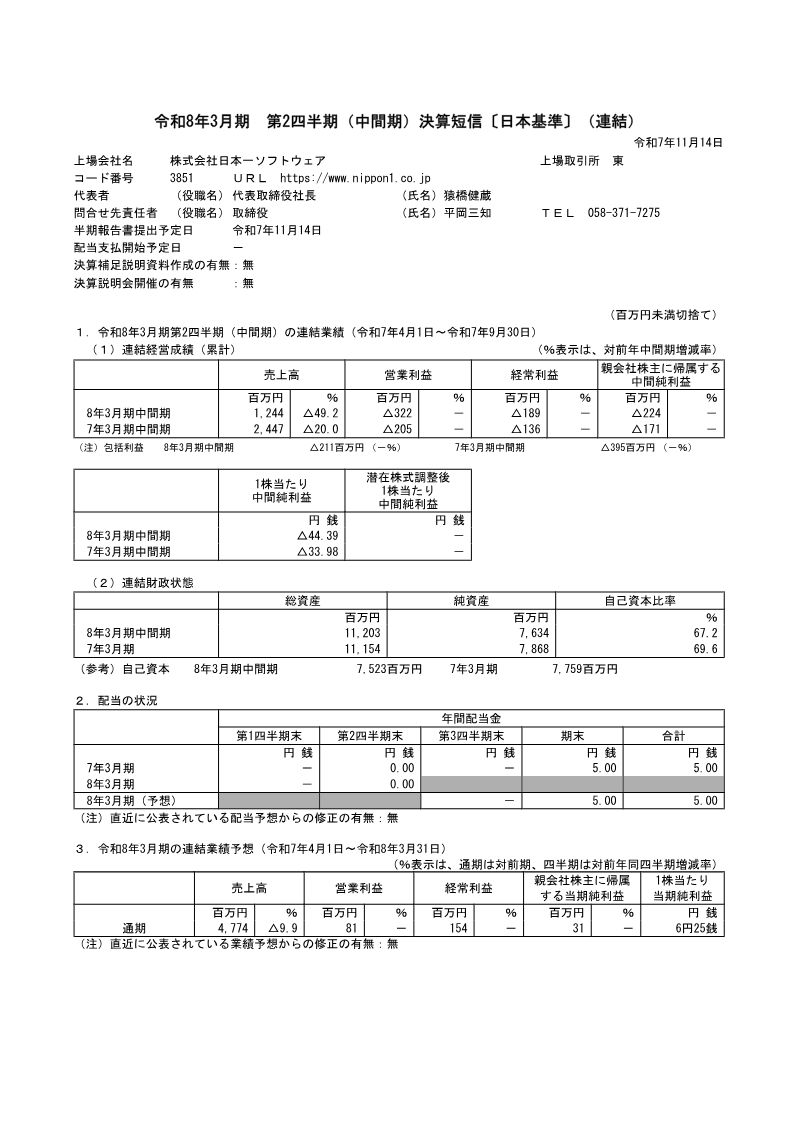

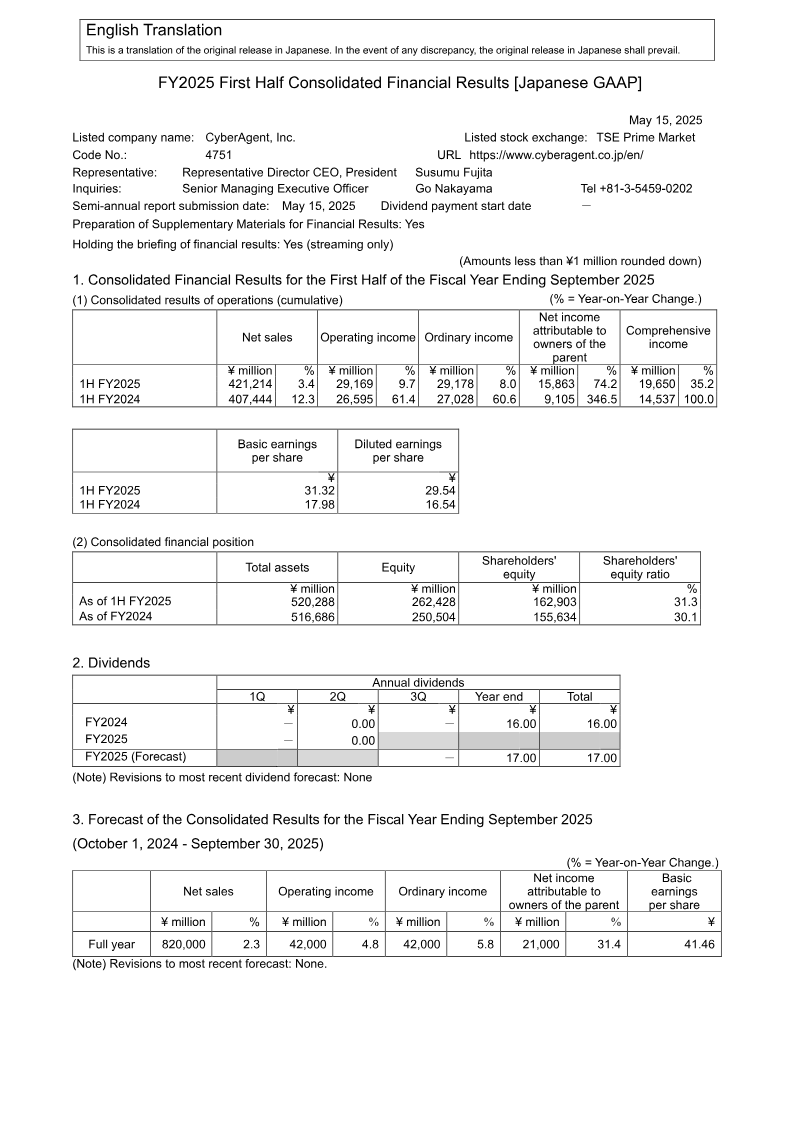

Nintendo experienced a significant financial contraction in the first nine months of FY2025, with net sales falling 31.4% to ¥956.2 billion and operating profit dropping 46.7% to ¥247.5 billion compared to the same period last year.

The core video game segment, which accounts for the vast majority of revenue, saw a 31.7% decline, driven by a 30.6% drop in hardware unit sales.

Despite the overall hardware and software downturn, digital sales increased their share of total software revenue from 48.1% to 51.0%.

The 'Other' revenue category, encompassing merchandise, official stores, and playing cards, was the only major segment to show growth, rising 27.6% year-over-year.

International markets became increasingly critical to Nintendo's revenue mix, with the proportion of sales generated outside Japan rising to 76.5%, up from 71.5% in the previous year.

Foreign exchange impacts were notable, as the average USD/JPY exchange rate weakened from ¥143.22 to ¥152.45, contributing to the shifting financial landscape.

**Nintendo Co., Ltd. – FY 2025 Q1‑Q3 Financial Results (Explanatory Material)** *Prepared 4 Feb 2025 – covering the period 1 Apr 2024 – 31 Dec 2024 (FY 25 Q1‑Q3)*

---

## 1. Core Financial Highlights (FY 24 Q1‑Q3 vs. FY 25 Q1‑Q3)

| Metric | FY 24 Q1‑Q3 | FY 25 Q1‑Q3 | YoY Δ | |--------|------------|------------|-------| | **Net sales** | ¥1,394.7 bn | ¥956.2 bn | **‑31.4 %** | | **Operating profit** | ¥464.4 bn | ¥247.5 bn | **‑46.7 %** | | **Operating profit margin** | 33.3 % | 25.9 % | **‑7.4 pts** | | **Ordinary profit** | ¥567.3 bn | ¥327.1 bn | **‑42.3 %** | | **Net profit** (profit attributable to owners) | ¥408.0 bn | ¥237.1 bn | **‑41.9 %** | | **Net profit margin** | 29.3 % | 24.8 % | **‑4.5 pts** |

*The decline is driven primarily by weaker hardware and software sales, a shift toward a higher share of “Other” (merchandise) revenue, and a less favorable foreign‑exchange environment.*

---

## 2. Revenue Mix

| Category (FY 24 Q1‑Q3) | FY 25 Q1‑Q3 | YoY Δ | |------------------------|------------|-------| | **Dedicated video‑game platform** (hardware + software + accessories) | ¥895.5 bn | **‑31.7 %** | | – Hardware | ¥895.5 bn × 46.1 % ≈ ¥413 bn | **‑30.6 %** (units) | | – Software (first‑party) | ¥895.5 bn × 73.4 % ≈ ¥658 bn | **‑9.1 pts** in share | | **Mobile / IP‑related income** | ¥49.7 bn | **‑33.9 %** | | **Other (merchandise, official stores, playing cards)** | ¥10.9 bn | **+27.6 %** | | **Proportion of sales outside Japan** | 76.5 % (FY 25) | up from 71.5 % (FY 24) |

*Digital sales grew as a share of software revenue (48.1 % → 51.0 %). The average USD/JPY exchange rate rose from ¥143.22 to ¥152.45, adding ¥9.23 per dollar to the yen‑denominated results.*

---

## 3. Cost Structure

| Item | FY 24 Q1‑Q3 | FY 25 Q1‑Q3 | YoY Δ | |------|------------|------------|-------| | **SG&A expenses** | ¥