White Paper on Global Mobile Games 2021

Jan 202163 pages10k words

Summary

The 2021 mobile gaming landscape was defined by a transition toward creative-led advertising strategies necessitated by rising acquisition costs and shifting privacy regulations. As iOS privacy changes prompted a strategic pivot toward Android platforms, the industry experienced a 200% surge in ad creatives and a 34% year-over-year increase in CPMs on major platforms like Meta. With the United States emerging as the most expensive market at an average CPM of $28.18, advertisers increasingly prioritized data-driven optimization and regional targeting to maintain return on investment amidst a broader 5% slowdown in total advertiser market growth.

While casual and puzzle games maintained the highest volume of individual advertisers globally, RPGs consistently dominated in total creative output across key regions, including Southeast Asia, Hong Kong, Macao, and Taiwan. To combat market saturation, developers shifted toward high-engagement formats, specifically vertical video ads exceeding 30 seconds and playable end cards. These creative strategies, often incorporating celebrity endorsements and real-people trailers, became essential tools for driving conversions in a competitive environment where traditional tracking methods faced significant headwinds.

Looking toward future growth, the industry is increasingly focused on globalization and the refinement of hybrid monetization models. Developers are diversifying revenue streams by integrating NFTs and combining traditional in-app purchases with ad-based structures. Furthermore, the adoption of privacy-compliant user acquisition, such as early SKAN testing and AI-driven optimization, has become a prerequisite for success. As companies expand into emerging markets like the Middle East and the CIS, the combination of M&A activity, social feature integration, and sophisticated monetization frameworks will remain central to navigating the complexities of the post-privacy mobile ecosystem.

Pages

Insights

- Rising acquisition costs and iOS privacy regulations triggered a 200% surge in ad creatives and a 34% year-over-year increase in CPMs on platforms like Meta.

- The United States became the most expensive market for mobile advertising, reaching an average CPM of $28.18.

- Total advertiser market growth slowed by 5% in 2021, forcing developers to prioritize data-driven optimization and regional targeting to protect ROI.

- While casual and puzzle games lead in advertiser volume, RPGs dominate total creative output in key regions including Southeast Asia, Hong Kong, Macao, and Taiwan.

- Developers are countering market saturation by adopting high-engagement formats, such as vertical video ads longer than 30 seconds and playable end cards featuring celebrity endorsements.

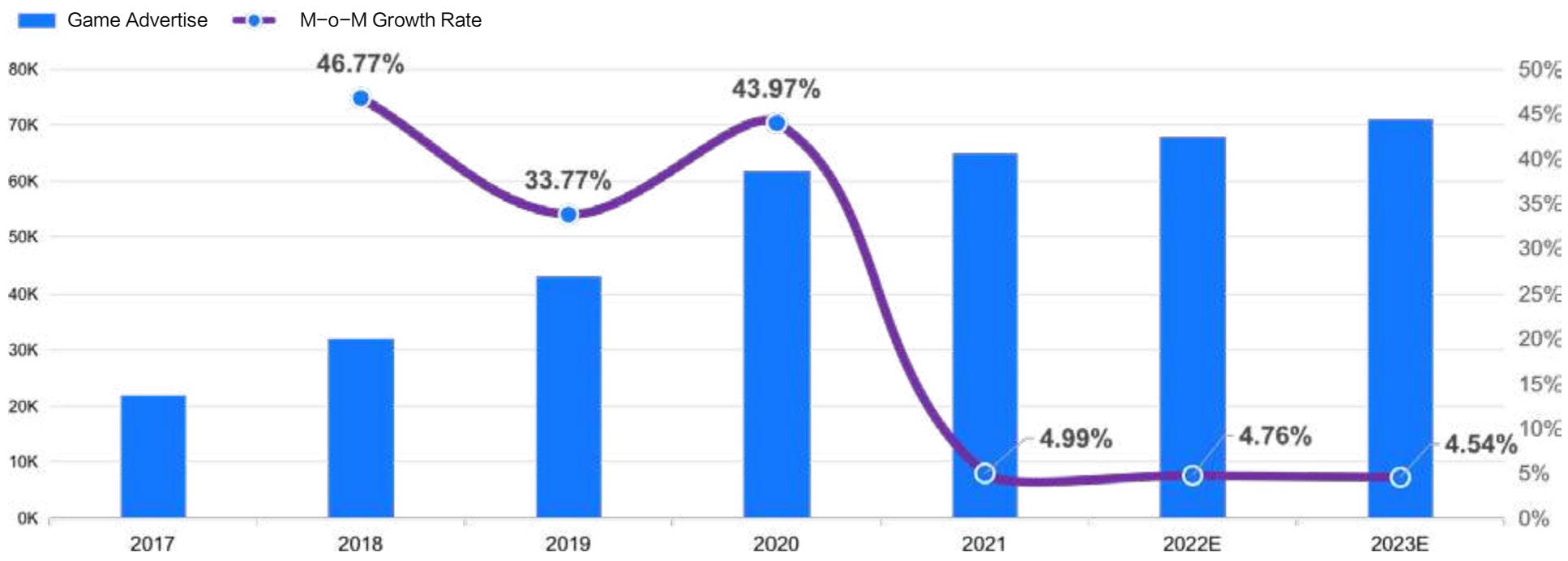

This chart illustrates the historical and projected growth of "Game Advertise" spending from 2017 to 2023, showing a steady increase in total expenditure alongside a significant decline in the month-over-month (M-o-M) growth rate after 2020.