Related Documents

Report

Global Sports Tech Market Report H1 2025

In the first half of 2025 the global sports‑technology sector recorded approximately $52 billion in announced or closed transactions, underscoring a rapid acceleration of both merger‑and‑acquisition activity and capital raising. Roughly $32 billion stemmed from 233 M&A deals, while a record‑high $6.6 billion was secured through 239 private‑placement rounds, more than 80 % of which involved early‑stage companies. The capital influx was driven by a mix of strategic consolidations—most notably TSG Consumer’s $1.5 billion acquisition of EOS Fitness and RTL’s $613 million purchase of Sky Deutschland—alongside a wave of targeted investments such as Valeas’s $110 million majority stake in Ticketmanager, Genstar’s acquisition of Playmetrics for integration with Stack Sports, and IMG’s takeover of SportsRecruits. Deal multiples varied across subsectors, reflecting divergent growth trajectories within wearables, fan‑engagement platforms, and performance‑analytics solutions. Geographically, the activity spanned North America, Europe and emerging markets, with transaction processing centralized through Drake Star Securities LLC in the United States and its UK affiliate, Drake Star UK Limited, both operating under FINRA regulation and SIPC membership. This infrastructure ensures compliance and investor protection for institutional participants. The concentration of early‑stage financing and the prevalence of large‑scale consolidations together signal a market transitioning from fragmented innovation toward integrated platforms capable of delivering end‑to‑end sports experiences. The data suggest that investors and strategic acquirers view the sector as a high‑growth arena, positioning it for continued expansion and deeper consolidation throughout the remainder of 2025.

Drake Star PartnersJan 2025

Report

Sports Tech Market 2025

The 2025 sports‑technology market experienced an unprecedented surge of private capital, with roughly 500 announced transactions totaling $14.3 billion. Early‑stage investments alone contributed about $8.8 billion, underscoring a robust pipeline of emerging innovators and a strong appetite among venture investors for nascent solutions across performance analytics, fan engagement, and digital infrastructure. This influx of funding reflects a broader confidence in the sector’s growth trajectory and its expanding role within the global sports ecosystem. Concurrently, the year was marked by a wave of mega‑valuations and record‑size mergers and acquisitions, most prominently the $10 billion acquisition of the Los Angeles Lakers and the $6.1 billion purchase of the Boston Celtics. These franchise deals, together with a $76 billion NBA media‑rights package, illustrate the escalating financial stakes attached to elite sports properties and the premium placed on content distribution platforms. Valuation metrics for traditional sports‑tech firms stabilized around an average EV/EBITDA multiple of 4.2× and a revenue multiple near 13×, indicating a mature market where profitability and top‑line growth are increasingly scrutinized by investors. Overall, the analysis captures a market that is both capital‑intensive and consolidation‑driven, with the United States serving as the focal point for high‑profile transactions while broader global trends echo similar patterns of investment and valuation. The data suggest that continued inflows of private capital, coupled with strategic M&A activity, will shape the competitive landscape and set valuation benchmarks for the next phase of sports‑technology development.

Drake Star PartnersJan 2025

Financial

Global Gaming Report Q1 2024

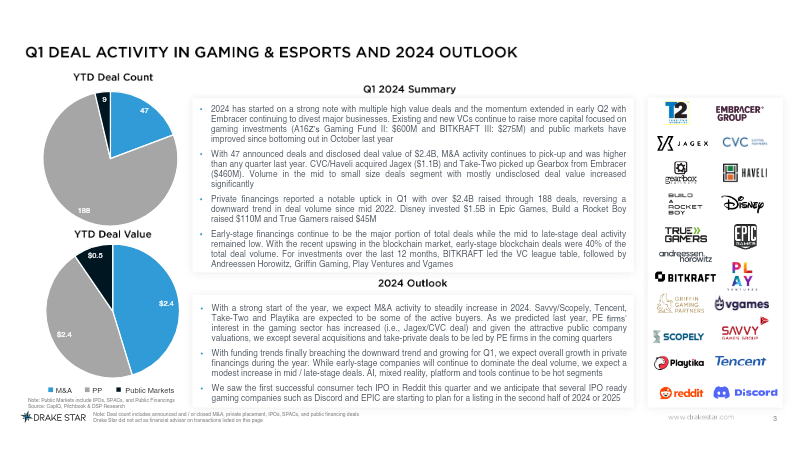

The first quarter of 2024 marked a pronounced revival in the gaming industry’s investment climate, underscoring a dual narrative of heightened deal activity and divergent financial performance across sub‑segments. Forty‑seven announced mergers and acquisitions generated $2.4 billion in disclosed value, while private‑equity financing matched that amount across 188 transactions, with early‑stage rounds remaining predominant. Notably, blockchain‑focused early‑stage deals accounted for 40 % of total deal volume, reflecting growing confidence in decentralized gaming models. Flagship transactions such as CVC and Haveli’s $1.1 billion acquisition of Jagex and Take‑Two’s $460 million purchase highlighted the scale of capital flowing into established IP owners. A comparative analysis of valuation multiples and revenue trajectories revealed a stark split between hardware‑platform and ad‑tech firms versus traditional game publishers. Companies like NVIDIA (EV/EBITDA≈36×, revenue $2.2 bn) and Applovin (EV/EBITDA≈7.8×, revenue $22.8 bn) posted double‑digit revenue growth and commanded premium multiples, whereas publishers such as Roblox, Skillz, and Atari experienced revenue declines, losses, and modest valuations. Exceptional upside emerged for firms like Wemade (+140 %) and Konami (+79 %), while Embracer suffered a steep 54 % contraction. Overall, the data suggest that capital is increasingly gravitating toward technology‑enabled and blockchain‑centric ventures, while legacy publishing entities confront earnings pressure and lower market confidence. The quarter’s dynamics point to a reshaping of the industry’s investment landscape, with future growth likely tied to the ability of traditional publishers to adapt to evolving platform and monetisation models.

Drake Star PartnersMar 2024

Financial

Global Gaming Report Q2 2024

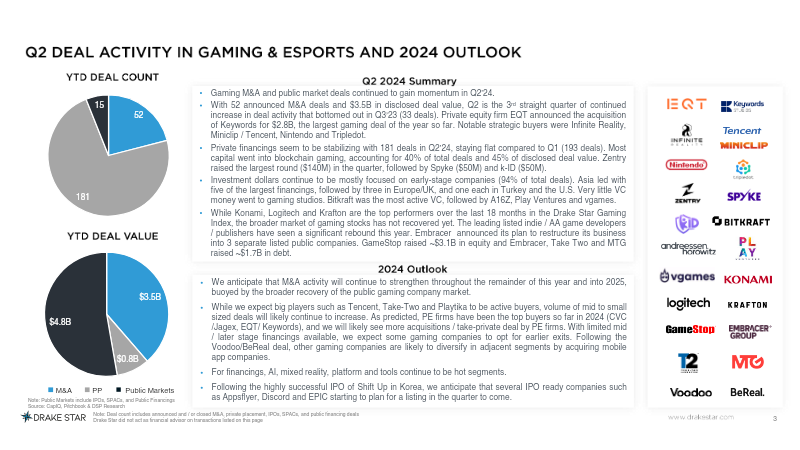

The second quarter of 2024 marked a pronounced resurgence in global gaming activity, driven by a surge in merger‑and‑acquisition activity and a revitalized indie and AA publishing landscape. Fifty‑two deals were announced, collectively valued at $3.5 billion, representing the strongest quarterly M&A performance since the third quarter of 2023. The most consequential transaction was EQT’s $2.8 billion acquisition of Keywords, underscoring the appetite of private‑equity and strategic investors such as Infinite Reality and Voodoo for high‑growth assets. Parallel to the consolidation trend, the indie and AA segment displayed robust expansion, with smaller publishers achieving double‑digit year‑to‑date revenue growth. Devolver Digital, Team 17 and tinyBuild each posted notable gains, while hardware and platform partners Logitech and KRAFTON recorded increases of 54.9 % and 53.7 % respectively. This rebound reflects heightened consumer demand for diversified experiences and the effectiveness of lean development models in capturing market share. Conversely, legacy publishers continued to confront headwinds, including declining engagement on older franchises and the pressure to adapt to evolving monetisation models. Their performance lagged behind the rapid growth observed among newer, agile studios, highlighting a sectoral shift toward innovative, lower‑cost production pipelines. Overall, the quarter illustrates a dual dynamic of intensified capital inflows and a competitive rebalancing that favours nimble developers. The data suggest that sustained investment and strategic acquisitions will likely shape the industry’s trajectory, while legacy entities must accelerate transformation to remain viable in an increasingly fragmented and fast‑moving market.

Drake Star PartnersJun 2024