Related Documents

Financial

Drake Star Global Gaming Report 2023

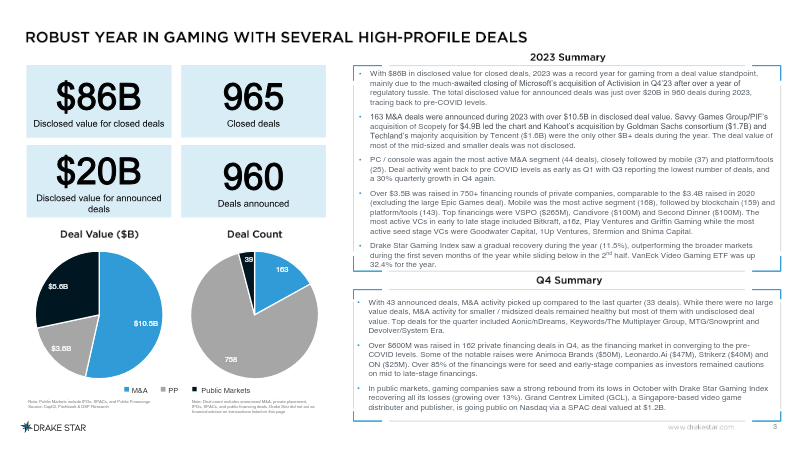

The global gaming industry experienced a significant transition in 2023, moving from the hyper-growth phase of the pandemic toward a normalized market environment characterized by strategic consolidation and targeted investment. While the year recorded a massive $86 billion in closed deal value, this figure was heavily skewed by the landmark Microsoft-Activision acquisition. Excluding such outliers, the broader landscape shifted toward smaller, mid-sized transactions, with 163 announced M&A deals totaling $10.5 billion and over $3.5 billion raised across 750 private financing rounds. PC and console segments dominated the M&A space, whereas mobile and blockchain ventures captured the majority of private financing volume. Strategic priorities for industry participants have evolved to emphasize the acquisition of intellectual property and the integration of transformative technologies. Firms such as Aonic Group, Modern Times Group, and Xsolla have actively expanded their portfolios to incorporate content creation tools, multiplayer capabilities, and virtual reality infrastructure. This focus on long-term value creation is further evidenced by the industry’s increasing interest in generative AI and Web3, which are viewed as critical drivers for future growth and operational efficiency. Looking ahead to 2024, the market is poised for a steady increase in activity as private equity firms capitalize on undervalued public companies and major industry players like Tencent, Sony, and Savvy Games Group continue their strategic investments. Although the current climate reflects a cautious approach to valuation, the outlook remains positive, with expectations for a resurgence in IPO activity as macroeconomic conditions stabilize. The sector is effectively pivoting toward a more disciplined investment model, prioritizing sustainable growth and technological integration to navigate the complexities of the global gaming ecosystem.

Drake Star PartnersJan 2023

Report

Drake Star Global Gaming Report Q3 2022

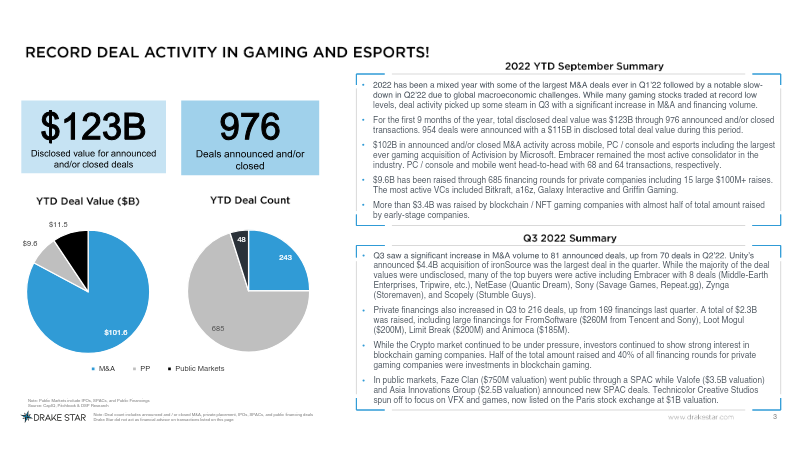

The global gaming industry experienced a year of unprecedented transaction volume through the first nine months of 2022, reaching a total disclosed deal value of $123 billion across 976 transactions. While a record-breaking first quarter gave way to a macroeconomic slowdown, the third quarter demonstrated resilience through a resurgence in activity, including 81 announced mergers and acquisitions and 216 private financings. This period was defined by a stark contrast between robust private investment and significant public market volatility, where major entities like Ubisoft and Roblox saw stock valuations decline by more than 45% since early 2021. Blockchain and Web3 gaming emerged as the primary catalysts for private capital, accounting for nearly half of all private financing value and 40% of total deal rounds in the third quarter. Significant capital infusions, such as Epic Games’ $2 billion round and the $4.5 billion raised for dedicated crypto gaming funds in May 2022, underscore the sector's shift toward decentralized models and "free-to-own" mechanics. Venture capital activity remained concentrated among top-tier firms like Andreessen Horowitz and Animoca Brands, even as the broader public market faced contraction and a quiet IPO landscape. Strategic consolidation remains a dominant trend as major players like Microsoft, Tencent, and Savvy Games Group leverage lower public valuations to pursue mid-sized acquisitions and take-private events. This shift toward consolidation is increasingly driven by a necessity for profitability and margin maintenance, particularly in high-growth regions like Southeast Asia and India, where strong revenue growth has been offset by negative EBITDA margins. Moving forward, the industry appears positioned for continued structural realignment as strategic buyers capitalize on market corrections to secure long-term intellectual property and technological infrastructure.

Drake Star PartnersSept 2022

Report

Global Gaming Report Q1 2023

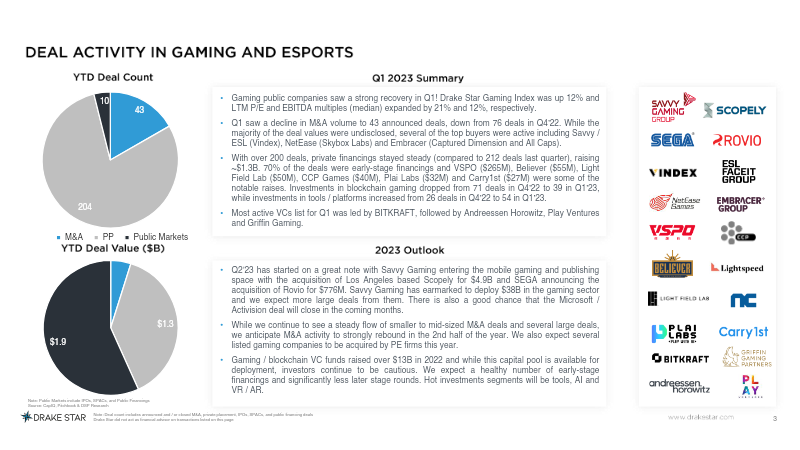

The global gaming industry entered 2023 showing signs of a robust public market recovery, evidenced by a 12% rise in the Drake Star Gaming Index and a notable expansion in valuation multiples. While the volume of mergers and acquisitions experienced a temporary dip to 43 deals, private financing remained resilient. Over 200 deals raised approximately $1.3 billion during the first quarter, driven primarily by early-stage investments. A strategic shift in investor interest became apparent as capital moved away from blockchain-centric projects toward gaming tools and artificial intelligence platforms. Investment activity was characterized by significant capital injections from major players, most notably Savvy Gaming Group’s $265 million investment in VSPO and Believer’s $55 million raise for open-world development. Venture capital firms such as BITKRAFT and Andreessen Horowitz maintained high deal volumes across PC, console, and platform segments. Despite the broader slowdown in consolidation, Embracer Group remained highly active, completing 18 deals totaling over $1.1 billion. Public market valuations revealed distinct regional and sectoral trends, with Japan and Korea-based developers commanding higher median EV/EBITDA multiples of 9.2x compared to the 5.7x seen in Western PC and console firms. The financial landscape remains complex and volatile, marked by modest median revenue growth of 1% for hardware and platforms and negative average profit margins across several segments. Regional disparities are particularly sharp in the Chinese market, where Shenzhen-listed firms maintain significantly higher valuation multiples than their counterparts. In the hardware sector, NVIDIA continues to dominate with a market capitalization exceeding $680 billion, despite facing substantial declines in EBITDA. Looking forward, the industry is positioned for a significant M&A rebound in the latter half of the year, supported by massive capital earmarks from sovereign wealth funds and high-profile acquisitions in the mobile and social gaming space.

Drake Star PartnersMar 2023

Financial

Global Gaming Report: Q3 2024

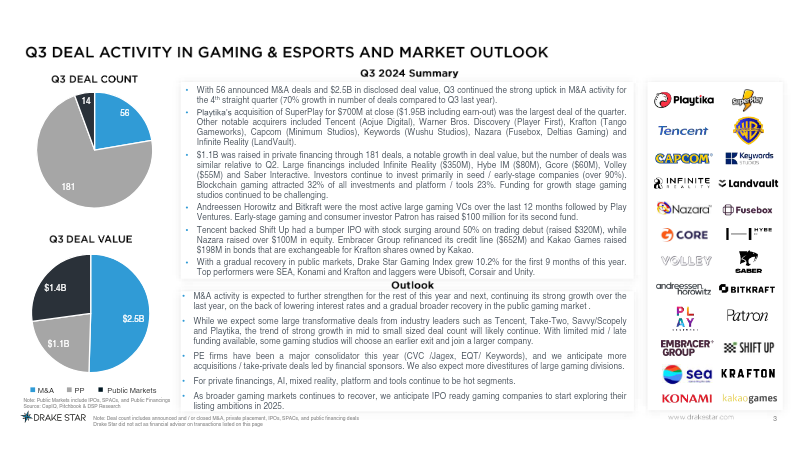

The global gaming industry experienced a significant resurgence in deal activity during the third quarter of 2024, characterized by a 70% year-over-year increase in merger and acquisition volume. With 56 announced deals totaling $2.5 billion in disclosed value, the market demonstrated a clear shift toward consolidation, headlined by Playtika’s $1.95 billion acquisition of SuperPlay. Private financing also showed resilience, reaching $1.18 billion across 181 deals. While growth-stage funding remains difficult to secure, early-stage investments flourished, particularly within the blockchain and platform tools sectors, which accounted for 32% and 23% of deal flow respectively. Investment leadership remains concentrated among a few key venture capital and strategic players. Andreessen Horowitz and BITKRAFT led the Series A and B stages with 15 deals each, while Animoca Brands dominated strategic investing with 38 transactions. This activity, coupled with Shift Up’s successful $320 million IPO, suggests a gradual recovery in public markets and sets an optimistic trajectory for 2025. Despite this momentum, valuation disparities persist across geographic and platform segments. PC and console-focused companies in North America and Europe command higher revenue multiples than their mobile counterparts, even when mobile firms report superior profit margins. The broader industry landscape is heavily influenced by the hardware and tools segment, where NVIDIA’s massive enterprise value and triple-digit revenue growth skew overall market data. In Asia, Japanese stalwarts like Sony and Nintendo continue to lead by market capitalization. These findings, compiled by Drake Star through June 2024, reflect a stabilizing ecosystem where strategic acquisitions and early-stage innovation are offsetting the lingering challenges of the growth-stage capital markets. The data indicates that while the industry is navigating complex valuation environments, the appetite for high-quality intellectual property and infrastructure remains robust.

Drake Star PartnersSept 2024