Related Documents

Report

Global Gaming Report H1 2022

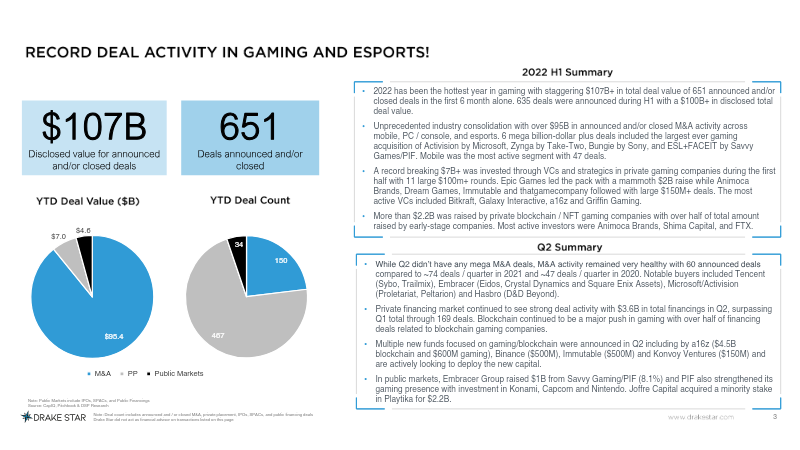

The first half of 2022 marked the most active period in the history of the gaming industry, characterized by unprecedented consolidation and record-breaking investment levels. Total deal value exceeded $107 billion across 651 transactions, with mergers and acquisitions accounting for $95 billion of that total. This surge was primarily driven by massive strategic consolidations, most notably Microsoft’s acquisition of Activision Blizzard and Take-Two’s purchase of Zynga. While the public markets faced significant headwinds and valuation corrections, the private sector remained resilient, securing $7 billion in financing across nearly 500 deals. Blockchain gaming and metaverse infrastructure emerged as the dominant catalysts for growth, representing over half of all financing transactions in the second quarter. This sector attracted more than $2.2 billion in funding, supported by the launch of multi-billion dollar funds from major venture capital firms. Despite the robust private activity, public gaming stocks largely underperformed, leading to a shift in investor focus toward high-quality, profitable targets. The absence of activity in the IPO and SPAC markets further underscored a transition toward private equity and strategic M&A as the primary vehicles for industry movement. The industry landscape is currently defined by a divergence between aggressive private investment and cautious public market sentiment. As valuation multiples adjust to new economic realities, the sector is positioned for a second half of the year focused on opportunistic acquisitions and potential take-private transactions. The continued integration of Web3 technologies and the entry of massive capital reserves suggest that while the pace of "mega deals" may fluctuate, the fundamental restructuring of the gaming ecosystem toward a consolidated, blockchain-integrated future remains the central trajectory for the global market.

Drake Star PartnersJul 2022

Report

Global Gaming Report 2022

The global gaming market achieved a record $127 billion in total deal value across 1,320 transactions in 2022, a surge primarily fueled by a threefold increase in merger and acquisition volume. This consolidation was headlined by transformative deals such as Microsoft’s $68.9 billion pending acquisition of Activision Blizzard and Take-Two’s $12.7 billion purchase of Zynga. While the PC, console, and platform tools segments attracted the highest volume of interest, major technology firms including Meta, Google, and Netflix simultaneously expanded their internal capabilities through strategic acquisitions in virtual reality, artificial intelligence, and independent studio development. Despite the record-breaking M&A activity, the broader financial landscape reflected significant volatility. Public gaming stocks experienced sharp declines, with many market capitalizations falling by more than 30%. Private financing deal counts rose by 29%, yet the total capital raised decreased to $11.1 billion as late-stage investments cooled. Blockchain gaming emerged as a particularly resilient sub-sector, securing $4 billion in funding across nearly 400 companies, supported by over $13 billion raised by specialized venture capital funds. Established industry leaders like Sony and Nintendo maintained robust EBITDA margins of 19.5% and 35.0% respectively, demonstrating operational stability amidst macroeconomic shifts. The industry is transitioning into a period of heavy consolidation and potential "taking private" transactions as companies capitalize on lower public valuations. Future growth and investment are expected to concentrate on augmented and virtual reality, AI-driven development tools, and mobile audience expansion. Furthermore, the emergence of the Savvy Gaming Group, backed by a $35 billion investment fund, signals a shift toward new geographic centers of influence. As the market matures, the first significant wave of consolidation within the blockchain gaming sector is anticipated, marking a move toward more sustainable, high-quality project development.

Drake Star PartnersJan 2023

Report

Global Gaming Report Q1 2023

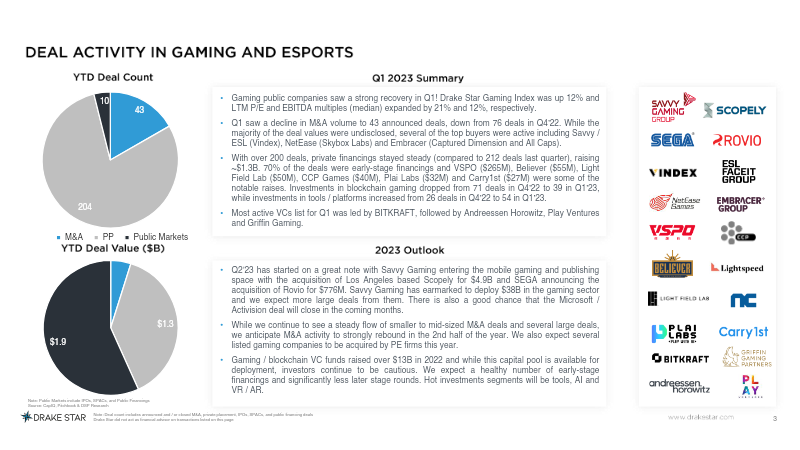

The global gaming industry entered 2023 showing signs of a robust public market recovery, evidenced by a 12% rise in the Drake Star Gaming Index and a notable expansion in valuation multiples. While the volume of mergers and acquisitions experienced a temporary dip to 43 deals, private financing remained resilient. Over 200 deals raised approximately $1.3 billion during the first quarter, driven primarily by early-stage investments. A strategic shift in investor interest became apparent as capital moved away from blockchain-centric projects toward gaming tools and artificial intelligence platforms. Investment activity was characterized by significant capital injections from major players, most notably Savvy Gaming Group’s $265 million investment in VSPO and Believer’s $55 million raise for open-world development. Venture capital firms such as BITKRAFT and Andreessen Horowitz maintained high deal volumes across PC, console, and platform segments. Despite the broader slowdown in consolidation, Embracer Group remained highly active, completing 18 deals totaling over $1.1 billion. Public market valuations revealed distinct regional and sectoral trends, with Japan and Korea-based developers commanding higher median EV/EBITDA multiples of 9.2x compared to the 5.7x seen in Western PC and console firms. The financial landscape remains complex and volatile, marked by modest median revenue growth of 1% for hardware and platforms and negative average profit margins across several segments. Regional disparities are particularly sharp in the Chinese market, where Shenzhen-listed firms maintain significantly higher valuation multiples than their counterparts. In the hardware sector, NVIDIA continues to dominate with a market capitalization exceeding $680 billion, despite facing substantial declines in EBITDA. Looking forward, the industry is positioned for a significant M&A rebound in the latter half of the year, supported by massive capital earmarks from sovereign wealth funds and high-profile acquisitions in the mobile and social gaming space.

Drake Star PartnersMar 2023

Financial

Global Gaming Report Q2 2024

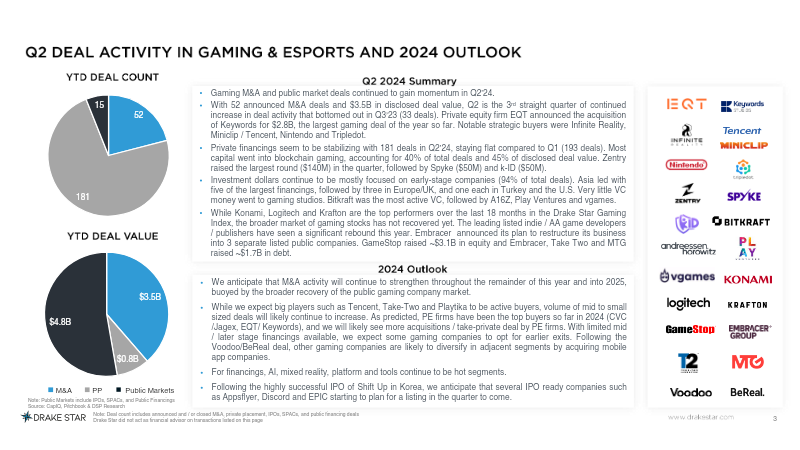

The second quarter of 2024 marked a pronounced resurgence in global gaming activity, driven by a surge in merger‑and‑acquisition activity and a revitalized indie and AA publishing landscape. Fifty‑two deals were announced, collectively valued at $3.5 billion, representing the strongest quarterly M&A performance since the third quarter of 2023. The most consequential transaction was EQT’s $2.8 billion acquisition of Keywords, underscoring the appetite of private‑equity and strategic investors such as Infinite Reality and Voodoo for high‑growth assets. Parallel to the consolidation trend, the indie and AA segment displayed robust expansion, with smaller publishers achieving double‑digit year‑to‑date revenue growth. Devolver Digital, Team 17 and tinyBuild each posted notable gains, while hardware and platform partners Logitech and KRAFTON recorded increases of 54.9 % and 53.7 % respectively. This rebound reflects heightened consumer demand for diversified experiences and the effectiveness of lean development models in capturing market share. Conversely, legacy publishers continued to confront headwinds, including declining engagement on older franchises and the pressure to adapt to evolving monetisation models. Their performance lagged behind the rapid growth observed among newer, agile studios, highlighting a sectoral shift toward innovative, lower‑cost production pipelines. Overall, the quarter illustrates a dual dynamic of intensified capital inflows and a competitive rebalancing that favours nimble developers. The data suggest that sustained investment and strategic acquisitions will likely shape the industry’s trajectory, while legacy entities must accelerate transformation to remain viable in an increasingly fragmented and fast‑moving market.

Drake Star PartnersJun 2024