30 results · 0.8s

Jan 2023

From Hyper to Hybrid: Hypercasual Gaming Trends 2023

Tenjin

Report27 pages

Jan 2025

2025 State of Mobile Gaming: In-App Purchase Trends of Leading Apps

Moloco

Report28 pages

Jan 2024

2023 Global Mobile Games Marketing Trends White Paper

SocialPeta

Report78 pages

Jan 2023

The State of Mobile Gaming in India: A Look at India's Casual, Hyper-Casual, and Real Money Gaming App Industry Trends

MoEngage

Report25 pages

Jan 2022

Unity Gaming Report 2022

Unity

Report40 pages

Jan 2020

Mobile Ad Creative Index 2020

Liftoff

Report47 pages

Oct 2023

Leveling Up: State of India Gaming FY'23

Lumikai, Lumikai Investment Advisors

Report12 pages

Jan 2022

The State of Mobile Game and App Markets: H1 2022

AdQuantum, SocialPeta

Report42 pages

Jan 2021

The African Mobile Apps Landscape (2021)

AppsFlyer

Report15 pages

Aug 2021

Mobile Game Genre Report: Puzzle Games

Newzoo, Pangle

Report26 pages

Mar 2024

Mistplay Mobile Gaming Spender Report 2024: Decoding Mobile IAP Spenders

Mistplay

Report33 pages

Jan 2021

The State of Mobile Gaming 2021

Sensor Tower

Report78 pages

Mar 2024

The Gaming App Insights Report: Unlocking Growth Opportunities for Mobile Marketers

Adjust

Report43 pages

Jan 2025

From Games to the Big Screen: The Impact of IP Across Platforms

Sensor Tower

Report6 pages

State of Mobile 2025: Why Community Wins on Mobile

Reddit, Adjust, Sensor Tower

Report29 pages

Jan 2019

Mobile Gaming Apps Report: 2019 User Acquisition Trends & Benchmarks

Newzoo

Report52 pages

Sep 2022

The State of Social Apps in Europe 2022

Sensor Tower

Report29 pages

Jun 2021

India: Mobile Market Spotlight: A Booming Mobile Economy

data.ai

Report40 pages

Jan 2025

Mobile Monetization Report 2025

AppMagic

Report61 pages

Jan 2026

State of India Mobile App Market 2026 Report

Sensor Tower

Report66 pages

Dec 2024

Digital Market Index: Q4 2024

Sensor Tower

Report46 pages

Jan 2023

5 Mobile App Predictions for 2024

data.ai

Report14 pages

Jun 2022

Innovative Monetization Features Snapshot Report June 2022

GameRefinery

Report35 pages

Jan 2023

From Hyper to Hybrid: 2023 Follow-up

Tenjin

Report11 pages

Jan 2023

Mobile Gaming Loyalty Report 2023

Mistplay

Report32 pages

Jan 2020

From Playing to Paying: The Art of Monetizing Games in Asia

Niko Partners

Report15 pages

Jan 2025

State of Mobile 2025: TikTok Edition

Sensor Tower

Report80 pages

May 2025

2025 GDC Trends Report: Connecting the World Through Games

Game Developers Conference

Report37 pages

Jan 2024

Levelling Up: State of India Interactive Media and Gaming Research FY24

Lumikai

Report15 pages

Jan 2024

Global Mobile Gaming Industry Outlook 2024

Sensor Tower

Report25 pages

From Hyper to Hybrid: Hypercasual Gaming Trends 2023

Jan 202327 pages1k words

Summary

The mobile gaming landscape is undergoing a significant structural shift as developers transition from hyper-casual models toward hybrid-casual strategies. This evolution is driven by a marked decline in ad revenue profitability, influenced by the implementation of App Tracking Transparency on iOS, shifting post-pandemic user behaviors, and increased selectivity from major publishers. To maintain sustainability, developers are increasingly integrating in-app purchases and meta-gameplay components into their titles while opting for self-publishing models to retain greater control over their assets.

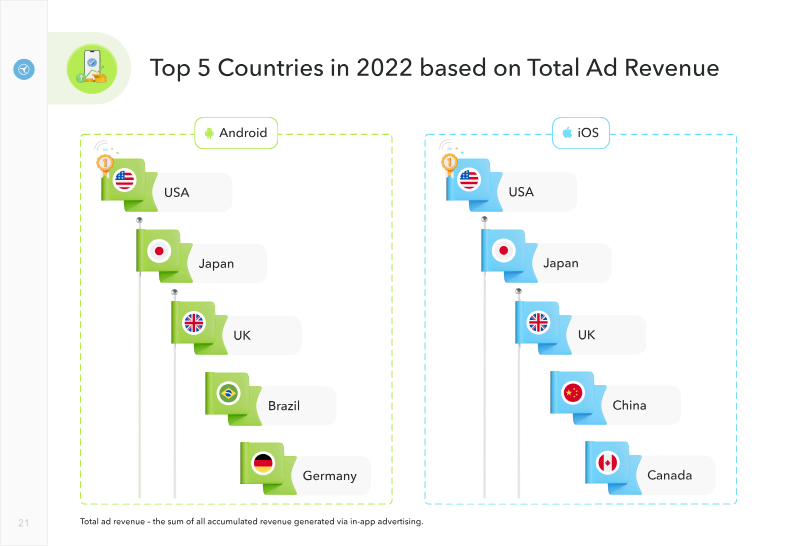

Data from 2022 reveals a downward trend in ad impressions and eCPMs across both Android and iOS platforms. Conversely, the volume of in-app purchases grew on both operating systems, signaling a successful pivot toward diversified monetization. Geographically, the United States remains the dominant market, ranking first for both ad revenue and in-app purchases across platforms. India emerged as the leading territory for total installs on Android, highlighting the importance of emerging markets for scale, even as monetization remains concentrated in Tier 1 regions.

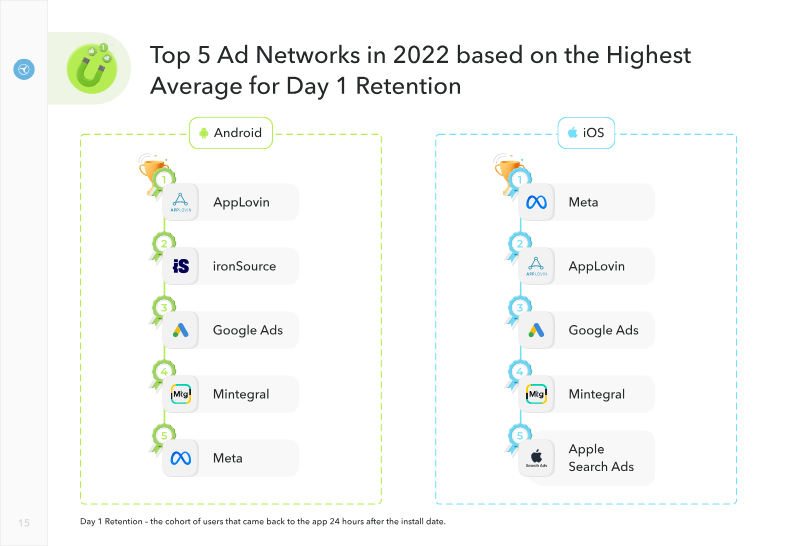

The competitive landscape for ad networks and monetization channels shows distinct leaders. Apple Search Ads dominates the iOS ecosystem, securing the top position in multiple categories including retention and lifetime value. On Android, AppLovin and ironSource lead the market. AppLovin specifically stands out as the top monetization channel by total ad revenue on both operating systems. For eCPM performance, Meta Audience Network and ironSource lead on Android and iOS respectively.

These findings are based on anonymized data collected throughout the 2022 calendar year, utilizing a weighted average methodology. The analysis focuses on high-scale performance, only including countries and ad networks that exceeded a threshold of 25 million installs. This comprehensive view underscores a broader industry movement where the traditional reliance on pure advertising is being replaced by a more balanced, hybrid approach to game design and revenue generation.

Pages

Insights

- The mobile gaming industry is shifting from hyper-casual to hybrid-casual models, driven by declining ad revenue profitability and the impact of iOS App Tracking Transparency.

- Developers are increasingly adopting in-app purchases and meta-gameplay components to replace the traditional reliance on pure advertising revenue.

- Data from 2022 shows a consistent downward trend in ad impressions and eCPMs across both Android and iOS platforms, while in-app purchase volume grew.

- The United States remains the primary market for both ad revenue and in-app purchases, while India leads in total Android installs, emphasizing the split between scale in emerging markets and monetization in Tier 1 regions.

- AppLovin is the leading monetization channel by total ad revenue across both iOS and Android platforms.

This image displays a line graph, likely from a game industry report, showing a trend over time. The green line with circular markers, each containing a small "tenjin" logo, indicates fluctuations in a particular metric, possibly user engagement, revenue, or downloads, with notable peaks and valleys throughout the observed period.