FinancialSquare Enix

Review of Operations: Square Enix Holdings Co., Ltd. Annual Report 2025

28 Feb 20266 pages~6 min full read

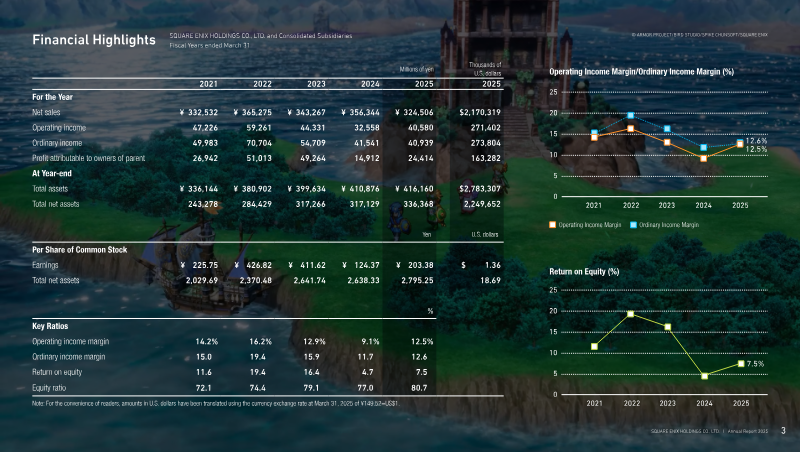

Square Enix achieved a 24.6% increase in operating income to ¥40,580 million for the fiscal year ending March 31, 2025, despite an 8.9% decline in net sales to ¥324,506 million.

The Digital Entertainment segment, representing 63.6% of total sales, grew operating income by 33.0% through cost-optimization, reduced advertising, and lower development amortization, even as segment revenue fell 16.8%.

Key intellectual property performance, specifically the 'Dragon Quest III HD-2D Remake' and 'Final Fantasy XIV: Dawntrail' expansion, served as the primary drivers for the company's improved profitability.

The Amusement segment recorded a 15.7% increase in sales and a 3.7% rise in operating income, bolstered by strong arcade machine distribution and same-store performance.

The smart device sub-segment underperformed due to the weakening of existing titles and the normalization of royalty revenues.

The Merchandising segment delivered a 7.2% increase in operating income, while the Publication segment saw a slight decline compared to the previous year's high baseline set by 'The Apothecary Diaries'.

The Square Enix Group’s operational review for the fiscal year ended March 31, 2025, reveals a period of strategic transition characterized by improved profitability despite a decline in overall revenue. Net sales fell 8.9% year-on-year to ¥324,506 million, yet operating income rose significantly by 24.6% to ¥40,580 million. This divergence was driven largely by cost-optimization efforts and the performance of key intellectual properties across the Digital Entertainment, Amusement, Publication, and Merchandising segments.

The Digital Entertainment segment, which accounts for 63.6% of net sales, saw revenue drop 16.8% due to a lighter release schedule compared to the previous year’s major launches. However, the segment’s operating income grew by 33.0%. This profitability was bolstered by the success of the Dragon Quest III HD-2D Remake and the Final Fantasy XIV: Dawntrail expansion, alongside reduced development cost amortization and lower advertising expenses. Conversely, the smart device sub-segment faced challenges as existing titles weakened and royalty revenues normalized.

Other business units showed mixed but generally stable results. The Amusement segment experienced growth in both sales and profits, rising 15.7% and 3.7% respectively, fueled by strong same-store sales and arcade machine distribution. The Publication segment saw a slight decline in performance, attributed to a high baseline set by the previous year’s hit adaptation of The Apothecary Diaries. Finally, the Merchandising segment remained a steady contributor, with a 7.2% increase in operating income supported by new character-based products. Overall, the Group’s results reflect a focus on enhancing margins and leveraging core IP through diverse entertainment formats.