FinancialNacon

First Half 2023/24 Sales: Nacon Financial Results

2 pages~4 min full read

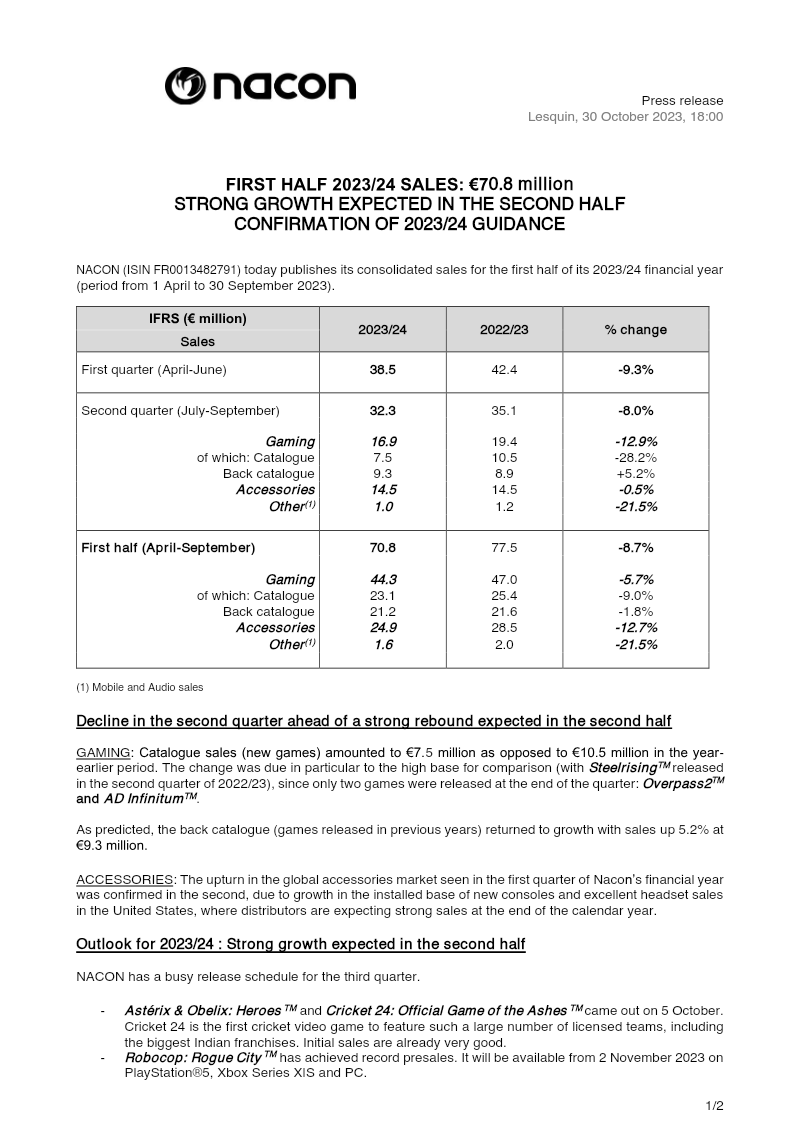

Nacon reported consolidated sales of €70.8 million for the first half of 2023/24, representing an 8.7% decline from the €77.5 million recorded in the same period last year.

See it on page 1Revenue fell across all primary segments, with accessories dropping 12.7% to €24.9 million and gaming revenue decreasing 5.7% to €44.3 million.

See it on page 1The company experienced a sharper sales decline in the first quarter (9.3%) compared to the second quarter (8.0%), attributed to a high base from the previous year and a limited release schedule.

See it on page 1Despite the overall downturn, Nacon reported a rebound in back-catalogue sales and improved accessories performance in the U.S. market, driven by new console installations and strong headset sales.

See it on page 1Nacon maintains its full-year 2023/24 guidance, anticipating a stronger second half supported by new releases such as 'Robocop: Rogue City', 'Cricket 24', and 'Astérix & Obelix: Heroes'.

See it on page 1Future growth is expected to be bolstered by new hardware launches, specifically the Revolution 5 Pro controller and the RIG 600 PRO headset.

See it on page 2Nacon reported consolidated sales of €70.8 million for the first half of its 2023/24 financial year, a decline of 8.7 % compared with €77.5 million in the same period a year earlier. Sales fell across all segments: gaming revenue dropped 5.7 % to €44.3 million, catalogue sales fell 9.0 % to €23.1 million, back‑catalogue sales slipped 1.8 % to €21.2 million, and accessories revenue fell 12.7 % to €24.9 million. Mobile and audio sales also contracted by 21.5 %. The first quarter saw a sharper decline (9.3 %) than the second quarter (8.0 %), reflecting a high base from 2022/23 and limited new releases in the latter half of the year.

Despite the downturn, Nacon highlighted a rebound in back‑catalogue sales and an upturn in accessories driven by new console installations and strong headset performance, particularly in the United States. The company’s release calendar for the third quarter includes high‑profile titles such as *Astérix & Obelix: Heroes*, *Cricket 24*, and *Robocop: Rogue City*, all of which have generated strong pre‑sales. Upcoming accessories, notably the Revolution 5 Pro controller and RIG 600 PRO headset, are expected to contribute further growth.

Nacon maintains its 2023/24 guidance, projecting robust sales and operating income in the second half of the year. The company’s integrated structure—combining 16 development studios, AA publishing, and premium peripheral design—supports its strategy to capitalize on new releases and accessory demand across 100 countries.