FinancialAkatsuki

Announcement of Consolidated Results for Fiscal Year Ended March 31, 2025

1 May 20252 pages~3 min full read

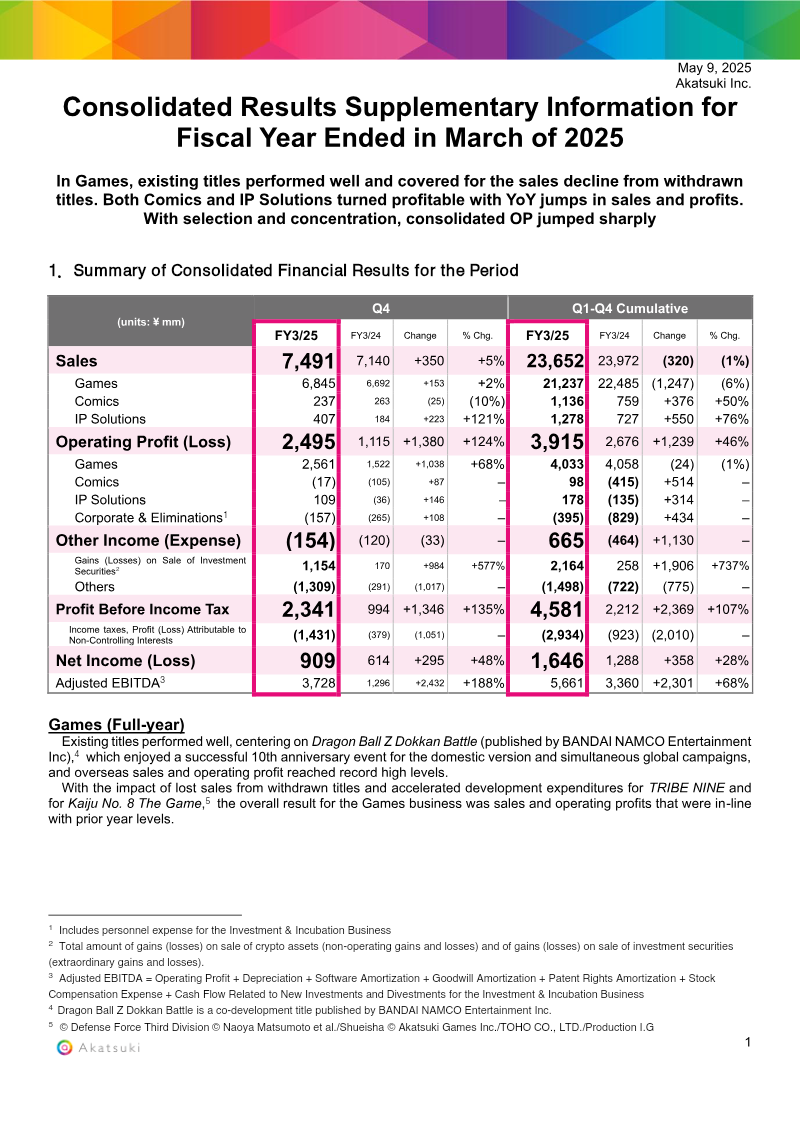

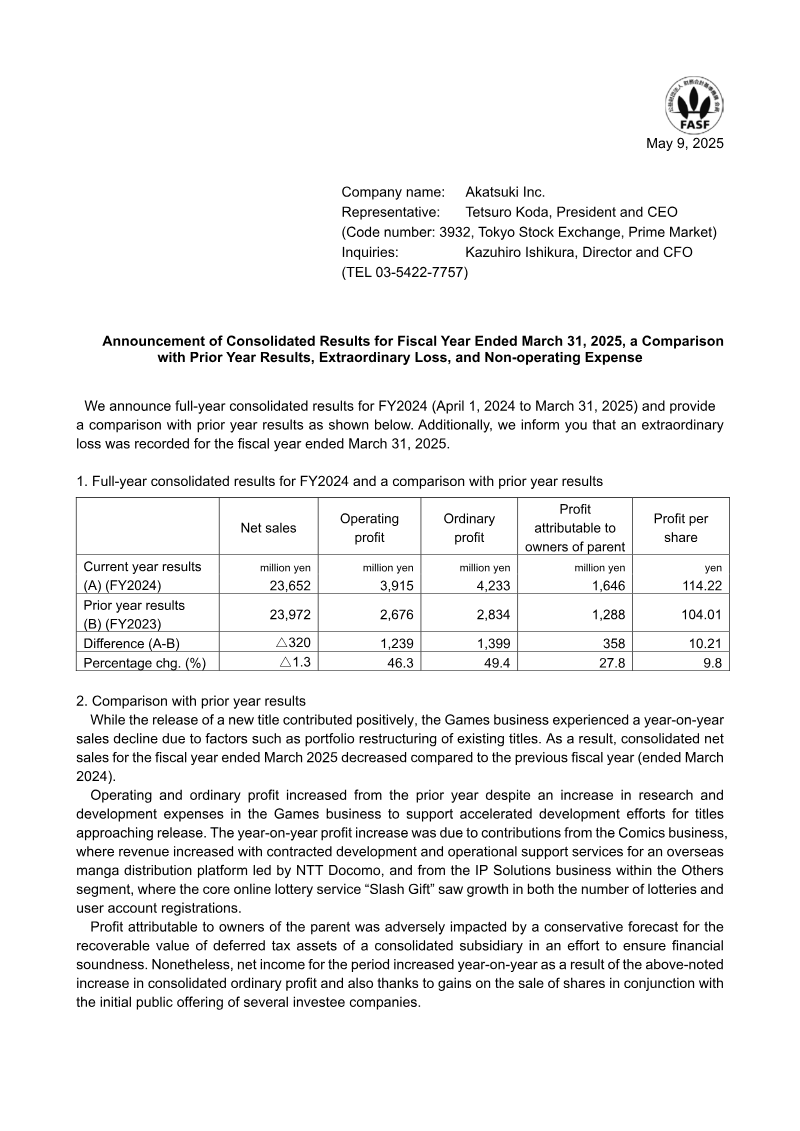

Akatsuki Inc. achieved significant profit growth for the fiscal year ended March 31, 2025, with operating profit rising 46.3% to 3,915 million yen and ordinary profit increasing 49.4% to 4,233 million yen.

See it on page 1Consolidated net sales contracted by 1.3% to 23,652 million yen, as portfolio restructuring in the core Games business offset revenue gains from new title releases.

See it on page 1Profit attributable to owners of the parent grew 27.8% to 1,646 million yen, supported by realized gains from the IPOs of several investee companies.

See it on page 1Diversification into non-gaming sectors drove margin improvements, specifically through development support for an overseas manga platform in the Comics segment and the expansion of the 'Slash Gift' online lottery service in the IP Solutions segment.

See it on page 1The company absorbed increased research and development expenses in the Games business by leveraging the profitability of its Comics and IP Solutions segments.

See it on page 1A consolidated extraordinary loss of 593 million yen was recorded for the valuation of investment securities, while non-consolidated provisions for doubtful accounts and valuation losses on affiliated company shares totaled over 8.2 billion yen.

See it on page 2Akatsuki Inc. reported a significant increase in profitability for the fiscal year ended March 31, 2025, despite a slight contraction in overall revenue. Consolidated net sales reached 23,652 million yen, representing a 1.3% decrease from the previous year. This decline was primarily driven by portfolio restructuring within the Games business, which offset the positive contributions from new title releases. However, operating profit rose by 46.3% to 3,915 million yen, and ordinary profit grew by 49.4% to 4,233 million yen. Profit attributable to owners of the parent also saw a 27.8% increase, totaling 1,646 million yen, resulting in a profit per share of 114.22 yen.

The improved profit margins were largely attributed to growth in the Comics and IP Solutions segments. The Comics business benefited from development and operational support for an overseas manga platform, while the IP Solutions segment saw expansion in its online lottery service, Slash Gift. These gains successfully mitigated increased research and development expenses within the Games business. Furthermore, the company realized gains from the sale of shares following the initial public offerings of several investee companies, which bolstered net income.

To ensure long-term financial soundness, the company recorded several one-time charges. On a consolidated basis, an extraordinary loss of 593 million yen was recognized for the valuation of investment securities. On a non-consolidated basis, the company recorded a 5,776 million yen provision for doubtful accounts and a 2,454 million yen loss on the valuation of shares in affiliated companies. While these non-consolidated figures are substantial, they represent internal assessments of subsidiary loans and investments and had a minimal impact on the final consolidated financial results for the fiscal year.